In today’s world, home security has become a top priority for homeowners looking to protect their property and loved ones. With burglaries and home invasions a constant concern, investing in a reliable home security system can provide invaluable peace of mind. Beyond deterring potential intruders, modern security systems offer many benefits, from protecting your home to integrating with smart technology for added convenience.

Types of Home Security Systems

1. Monitored Systems

Monitored home security systems are among the most comprehensive options available. These systems are professionally monitored 24/7, meaning that trained professionals will respond immediately if an alarm is triggered. The primary benefit of a monitored system is constant oversight, ensuring that emergency services are contacted even if you’re not home or unable to call for help. While these systems may come with higher installation and monthly fees, their reliability and fast response times make them ideal for homeowners seeking robust protection.

2. DIY Systems

DIY security systems are becoming increasingly popular for their affordability and ease of installation. These systems are typically wireless and come with customizable components, allowing homeowners to tailor the setup to their needs. While DIY systems generally don’t include professional monitoring, many offer remote monitoring through a mobile app, allowing you to monitor your home from anywhere. These systems are perfect for tech-savvy homeowners looking for flexibility and control over their security.

3. Wireless vs. Wired Systems

Wireless and wired home security systems each have their pros and cons. Wireless systems are easy to install, making them ideal for renters or homeowners who want a hassle-free setup. They are also portable, allowing them to be easily moved or expanded. However, they rely on Wi-Fi, which could be a vulnerability if the connection drops. On the other hand, wired systems offer more stable connections and don’t depend on wireless signals. Still, their installation is more complex, often requiring professional assistance and permanent fixtures within the home.

Features to Consider

When choosing a home security system, including essential components that provide enhanced protection is critical. Here are key features to keep in mind:

Cameras: Essential for monitoring entrances and vulnerable areas around your home.

Sensors: Placed on windows and doors to detect any unauthorized entry.

Alarms: Effective deterrents for burglars, alerting you and your neighbors of a break-in.

Smart Home Integration: Many systems can control locks, lights, and cameras remotely through a smartphone app, making it easier to monitor your home from anywhere.

Choosing the Right System

Several factors should guide your decision when selecting a home security system:

Budget: Systems vary widely in cost based on features and whether professional monitoring is included.

Home Size: The size of your home determines how many cameras and sensors you’ll need.

Neighborhood: Consider your neighborhood’s safety. Homes in higher-crime areas may require more advanced security features.

Comprehensive Detection: Look for systems that offer additional protection, such as smoke and carbon monoxide monitoring and burglary protection.

Secure Your Home with the Right System

Purchasing the right home security system involves understanding the options available and choosing one that fits your needs. Whether you opt for a monitored system or a DIY setup, the right system can help protect your home and family. As you explore your options, consider the features, installation process, and costs that make the most sense for your home. Prioritizing home security gives you peace of mind that your property is safe, whether at home or away. To learn how home security systems affect your insurance coverage, talk to one of our local insurance agents today.

Your Yard’s Health. The more the leaves pile up and begin to break down, the more difficult they’ll be to clear away. If it snows before you’ve had a chance to rid your yard of them, they’re likely to stay on your lawn all winter, where they’ll block sunlight and encourage the growth of mold and fungus on your lawn.After you’ve cleaned up the majority of the leaves, apply fertilizer to your lawn to help prevent winter damage and so that it revives quickly next spring.In addition to cleaning up your yard, don’t forget to harvest and cook your fall veggiesand plant your spring bulbs. You can also start bringing in your potted plants or flowers. If your annuals have already died, dispose of them and empty, clean and dry the pots before you put them away for use next spring.

Finally, drain your garden hoses and disconnect them from the outdoor spigots. Store them in a dry place to prevent freezing or cracking. Be sure to winterize your outdoor faucets and irrigation systems. You can even call in an expert to help you with this fall home prep.

5. Lighting

As the weather cools down, the days grow shorter and it gets dark earlier. If you don’t have outdoor lighting installed, consider making it a priority. After all, you don’t want to risk tripping when you take the dog out. Make sure to purchase products that are meant for outdoor use. Energy-efficient bulbs are a good option because they help you save money.

If you already have outdoor lighting installed, be sure to check that everything’s in working order.

6. Yard Equipment

To store your lawn mower until next spring, empty the fuel tank or add a fuel stabilizer to a full tank of fuel, change the oil and have the blades cleaned and sharpened. It’s also a good idea to remove the battery and stash it in a cool, dry place.

Service your snow blower so that it’s ready at a moment’s notice for unexpected winter weather. And if you have an emergency generator, test it out to make sure it’s in good working order. You don’t want to find out that your generator is out of order when you’re stuck in the middle of a storm with no electricity or heat.

7. Garage and Shed

Forget spring cleaning. Now is the perfect time to tidy up your garage or shed. Start by disposing of any liquids that might freeze, as well as unneeded flammable or hazardous materials.Clean, organize and put away your tools and equipment. Make room for your car in your garage so that you can safely pull it in during bad weather.

8. Summer Vehicles

Summer cars, ATVs, boats, golf carts and RVs should be serviced and stored for the winter. Change the oil, top off the gas tank (and add a fuel stabilizer) and cover the gaps through which rodents might be able to enter. And don’t forget to consider your vehicle insurance needs. If your car, for example, will be garaged all winter, you might be able to drop collision coverage, but it’s a good idea to maintain your comprehensive coverage should theft, fire or another type of non-collision damage occur.

9. Windows and Doors

Seal any gaps and cracks around your windows and doors with caulk, weather stripping or window insulator. Also seal any entry points for cable lines or phone lines — these are all exit points for your home’s warmth. And if you have reason to suspect severe winter weather may be headed your way, swap out your screens for storm windows and doors if you have them.

10. Safety Checks

Test your smoke and carbon monoxide alarms, test your fire extinguishers and review your emergency escape plans. If you don’t have any documented plans, now would be a good time to put them together and discuss them with your family.

11. Furnace

It’s a great idea to hire a professional to service your furnace. They can change the filter, make sure the moving parts are lubricated, inspect the burners and electrical connections, check for leaks, test safety features and ensure proper ventilation. You might be able to tackle some of these things yourself, but you’d risk doing them wrong, damaging your furnace and endangering your safety. For those reasons, it’s best to let a specialist handle this.

12. Fireplace

As the temperature drops, it’s crucial to follow fireplace safety tips. Hire a professional to check your fireplace and chimney and to remove any build-up. This person can also repair or replace the chimney cap if it is damaged or missing to prevent animals and debris from entering.

If yours is a wood-burning fireplace, stock up on firewood but store it at least 30 feet away from your home or any other structures. Seasoned hardwoods, such as oak, are best for firewood. And be sure to use a mesh metal screen or glass fireplace doors to prevent stray embers from escaping while your fireplace is in use.

13. Thermostat

If you haven’t already upgraded to a programmable thermostat, you should at least consider it. You can program it to lower the temperature while you’re asleep and when you’re not home, reducing your energy consumption and saving you money. And if you go away for the weekend, but forget to adjust the temperature before you leave, a lot of newer models—the so-called smart thermostats—will let you do so from your smartphone, tablet or computer.

14. Pantry

With the holidays just a few months away, now is a great time to clean out your pantry. Remove the boxes and cans so that you can vacuum up any loose crumbs to avoid providing a meal to critters that might get into your home looking for a good meal and a warm bed. Obviously, you’ll want to dispose of anything that’s expired. If you have unopened, unexpired items that you probably won’t get to in the next few months (such as ice tea or lemonade mix), consider donating them to your local food pantry.

Fall, especially in the Northeast, is breathtaking. And with some fall home prep you can get your house cold-weather ready while you enjoy the fleeting moments that make fall unique. In the process, not only will you be prepping your home for the coming winter, but you’ll also be mentally preparing yourself for the transition from heatwave to snowstorm.

Disclaimer: If you have questions or concerns regarding your policy, contact a Bolder Insurance Representative.

Life Insurance Corporation of India regularly adds more services to its online portal, which are more useful and now very important for the policyholders as they cannot move freely during this pandemic.

From 01/07/2020, Life Insurance Corporation of India has given the facility on its portal to register NEFT details in LIC online. You must not visit the LIC office to register the NEFT details. Now, within the safety of your home, you can write the NEFT details in LIC online.

इस पोस्ट को हिंदी में पढें: एलआईसी में एनईएफटी विवरण ऑनलाइन दर्ज करने के 7 चरण

Before registering the NEFT details in LIC online, you must have the following things with you to complete the process without any problem. First, you must be registered on the LIC portal to register the NEFT details. If you are not registered yet please read एलआईसी ई-सेवाओं के लिए रजिस्ट्रेशन कैसे करें? (How to register for LIC e-Services). We will proceed with the next part, assuming you are registered on the LIC e-Services portal. You must have the following things to complete the Process.

Scanned image of your CTS cheque (Please note that only a CTS cheque is accepted to register NEFT details in LIC online)

Scanned image of your PAN card.

If you want to update NEFT from the branch, click here to download the LIC NEFT form.

So let’s see the Process of How to register NEFT details in LIC online

Step 1: Log in to the LIC portal

Login to your LIC e-Services account using your LIC customer portal ID and Password; you can go to the LIC customer portal using this link.

Step 2: Select Service request to Register NEFT online

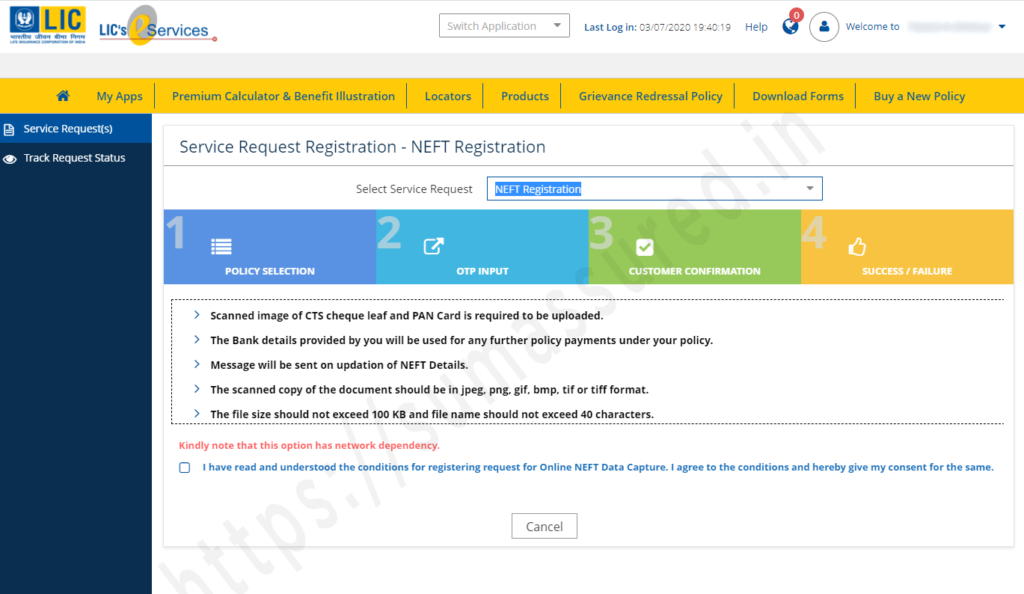

After you click the Service Request(s) button, you will be directed to the Service Request page to register a new request in your LIC policy. To register NEFT details in LIC online, click on the drop-down Select Service Request. You will see 7 options to choose from those is:

Premium Service Registration

Loan

Address Change

Change of Mode

NEFT Registration

Online ULIP fund switch

PAN data registration

So, today, we are looking for NEFT registration only. Don’t worry; we will discuss all the service requests in detail in my next posts. Anyways, click on NEFT Registration from the drop-down list.

When you select NEFT Registration from the drop-down menu, a piece of new information will appear on your page. Read it carefully; I have given it below for your ready reference to register NEFT details in LIC online

Read the conditions carefully, accept them, and proceed.

Step 3: Policy Selection for NEFT Registration

Please check the condition acceptance box thereafter, the Proceed button will appear on the screen. Click on the Proceed Button to go to the next step, i.e., the policy selection. On the next screen, you will see all the policies that do not have the NEFT details registered. Just select the policy in which you want to update the NEFT request.

There is no option to choose multiple policies to register the NEFT details. You must repeat the process for every policy you want to register the NEFT details online. A Proceed button will appear as soon as you select the policy displayed on the screen. Click the Proceed button for OTP validation to register NEFT details in LIC online.

Select the policy in which you want to register the NEFT details

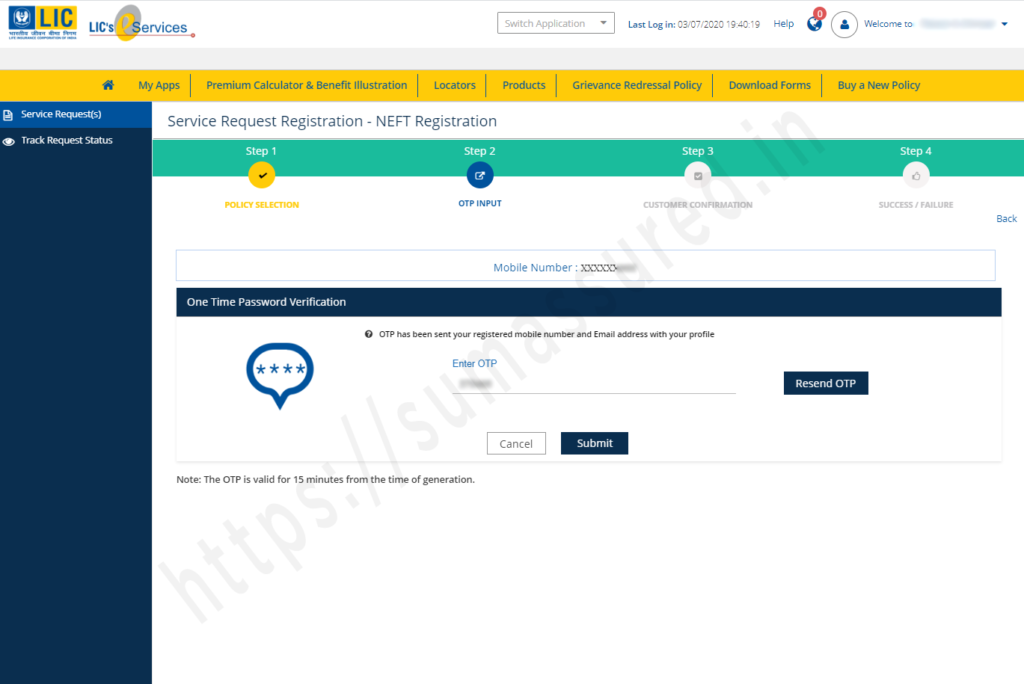

Step 4: OTP validation for verification register NEFT details in LIC online

Just click on the Proceed, and an OTP will be triggered on your mobile number registered in your LIC portal to register NEFT details in LIC online

Enter the OTP received on your mobile and click submit.

You will receive a 6-digit OTP on your registered mobile number. Just enter the OTP in the designated place and Click on submit. If, in any case, you do not receive OTP, press the Resend OTP button to resend the OTP on your mobile. Please note that you will receive a different OTP every time, so always enter the newest OTP to proceed further.

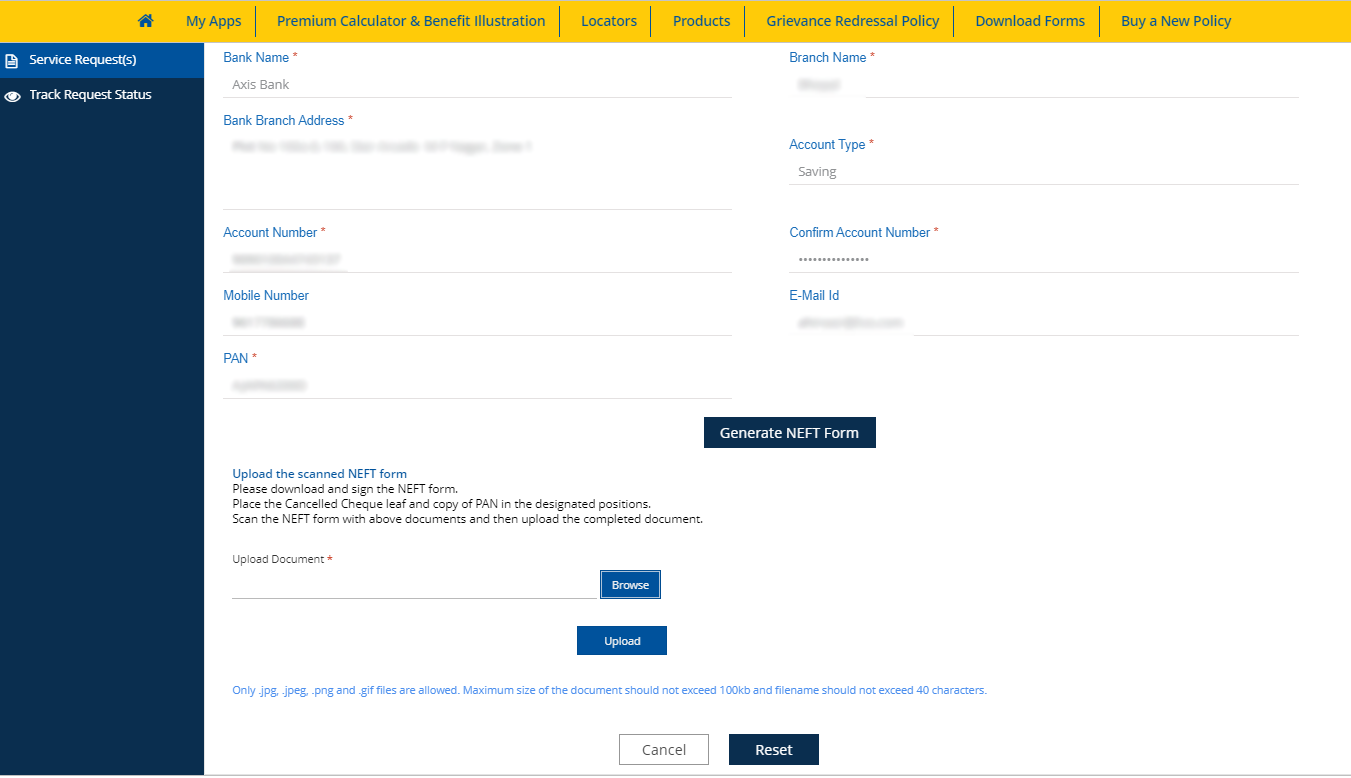

Step 5: Fill in your bank details

After the successful validation, you will be redirected to the page where you must give the bank details to register your policy. Your policy number and your name, as per your policy record, along with your registered mobile number and email ID, will be visible on the screen.

You must fill in the following details on this page to register NEFT details in LIC online.

Your bank IFSC code. An 11-digit code is specific to every bank branch. Please note that the first four letters of the IFS code are alphabets assigned to every bank and unique for every bank. 5th letter is 0 (Zero) by default. The following 6 letters can be numbers or alphabets. As soon as you enter the IFSC code of your bank branch, bank and branch details will be displayed on the screen; you do not have to fill in those details manually.

Select your account type from the drop-down list

Enter your bank account number

reconfirm the bank account number

enter your PAN number in the designated place

After entering all the details, hit the Save button to save the data. If you want to change the data and enter it again, click on the Reset button, and every detail filled by you will be removed. Enter the correct details again and click the Save button to register NEFT details in LIC online.

Fill in your bank details.

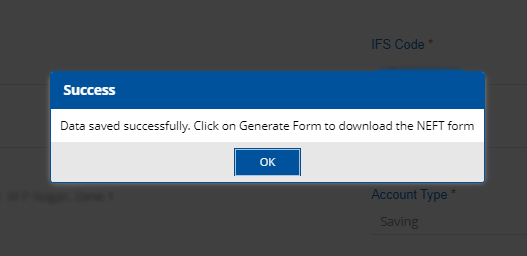

Step 6: Generate the NEFT form

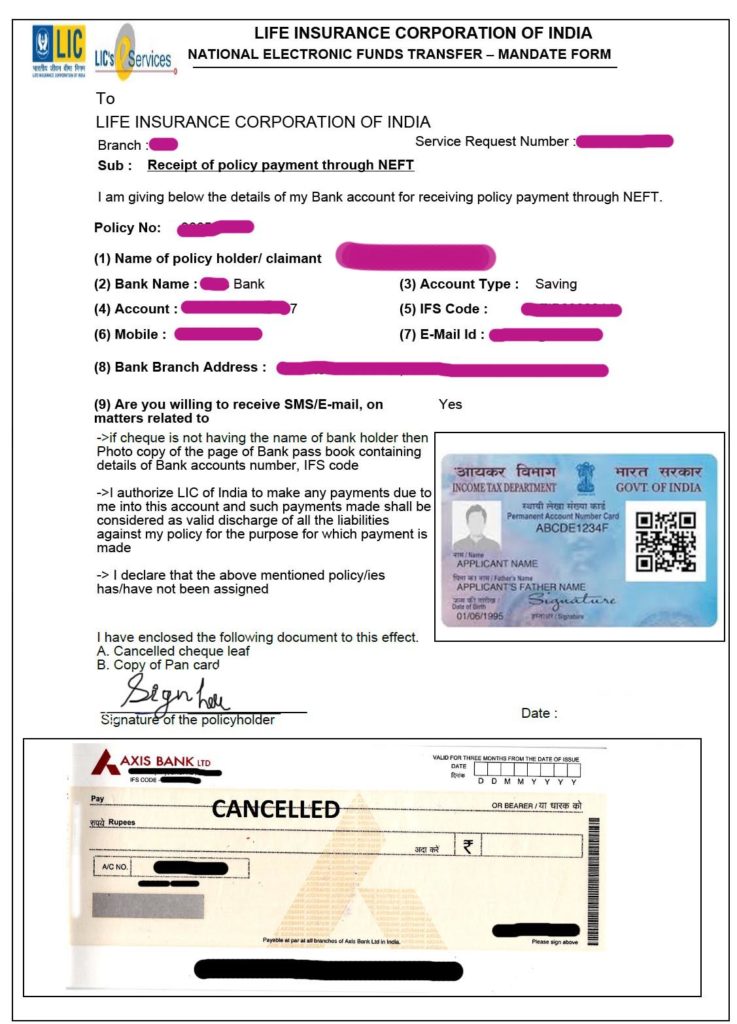

If all the data is correct, a Success message will be displayed on your screen below. Now, click OK to proceed further. On the next screen, you will see a new button at the bottom of the page: Generate NEFT Form. Click the button to generate the NEFT form to register NEFT details in LIC online. The Form contains all the details related to you ie your policy number, name, mobile number, email ID, and the bank details entered by you in the previous step. This form will also have two boxes exclusively for your Cheque and PAN card images.

Success message after error-free data entry.Click on Generate NEFT Form to download the form to register NEFT details in LIC online.

Take the printout of the form, sign and put the date on it. Now, either place your PAN card and CTS cheque in the designated place and scan the form or scan the form and place the already scanned images of the CTS cheque and PAN data in the designated places. See the complete form below to register NEFT details in LIC online(For security and privacy reasons, sensitive information is hidden)

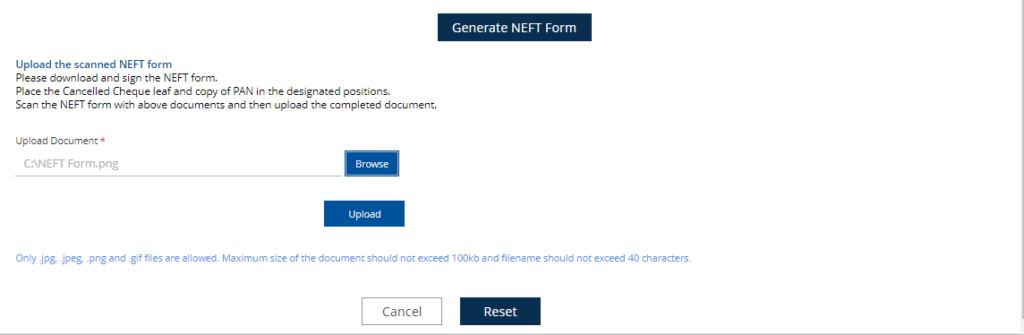

Step 7: Upload the NEFT form to register NEFT details

Scan the form and save it in one of these formats, i.e., JPG, PNG, or GIF file format, and upload it on the LIC portal. To upload the scanned NEFT form, click the Browse button on the page (see the screenshot below), select the scanned image, and hit the Upload button to upload the document. Please remember that a file larger than 100kb is not allowed, so keep it below 100kb size to register NEFT details in LIC online.

Upload the NEFT form.

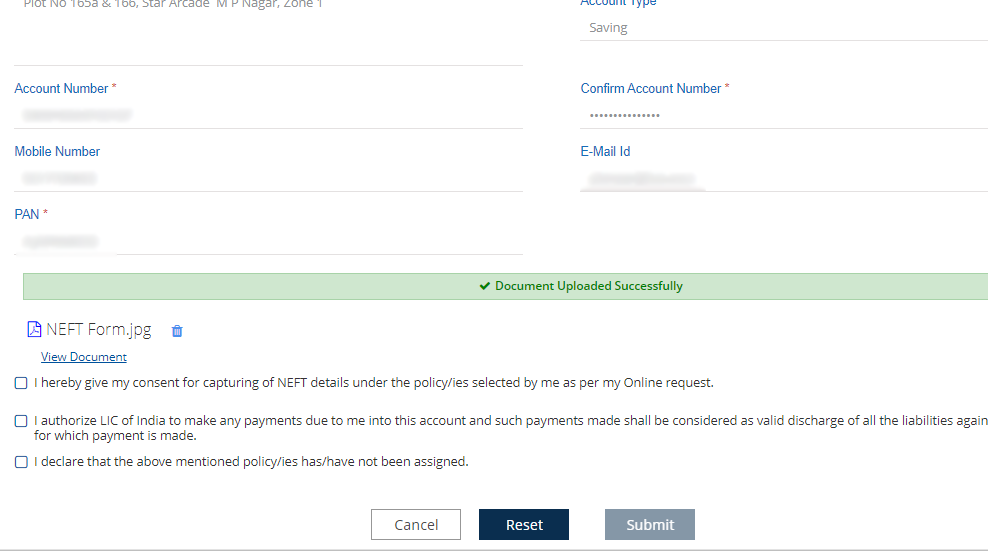

After the successful upload, a message “Document Uploaded Successfully.” Now read the statement below the message, check to mark them to accept them, and click the Submit button. Now, your Process is complete to register your NEFT in LIC online.

An email related to this will be sent to your registered email ID regarding the successful updation of your NEFT details in your policy. Repeat the process for all your policies to register the NEFT details in LIC online.

Your NEFT registration will not be successful until the LIC branch validates the documents uploaded by you. If it’s taking time, you can call the concerned branch and ask them to validate your NEFT request.

If you cannot do this process, you can submit the request offline in any LIC branch. You must fill out the NEFT Mandate form to register bank details in your LIC policy. Submit a cancelled cheque with the NEFT mandate form or a copy of the bank passbook. Click here to download the LIC NEFT Mandate form.

If you have any other LIC servicing questions, mail us at [email protected]. You can also comment below. Share if you liked this valuable information because Sharing is caring!

Read More:

मेरे क्रेडिट स्कोर सिबिल, और अन्य 3 ब्यूरो में भिन्न क्यों हैं?

Amazon, one of the world’s largest tech firms, has announced their decision to end their hybrid work policy in favor of returning to the office five days a week. This decision raises questions as to whether this will be the first of many tech industries abandoning flexible and hybrid schemes.

This move sparks several controversies in Singapore as the country has most recently adapted their policies on 4-day work weeks. In this article, we will look at the impact Amazon’s decision has on the industry and what it means to employee benefits moving forward.

What This Means for Amazon Employees

The recent announcement has sent waves down Amazon’s Singapore office, with employees expressing disappointment and concerns over the company’s decision as many have adapted to the flexibility of hybrid work.

The abrupt shift back to a full-time office setup also contradicts the prevailing trend of tech companies embracing remote and hybrid work arrangements worldwide.

How the Tech Industry Will be Affected

The decision made by Amazon could potentially set the precedent for other tech companies to follow suit. While large tech firms may not immediately enforce a full return to the office due to space constraints resulting from previous real estate reductions, it is anticipated that they may eventually move towards a more traditional in-office work model.

This shift can cause significant implications for talent retention and attraction within the industry. Whilst larger firms may not be affected as much with switching back to an office-based work arrangement, smaller firms may find it more challenging to compete for talent; as such, they may want to offer flexible work arrangements despite the new shift in the industry to remain competitive.

What Challenges Will This Bring?

Whilst there are arguments in favor of in-office work for fostering collaboration and strengthening company culture, others highlight the challenges associated with a full return to the office. Factors such as commute times, productivity, and work-life balance come into play, posing potential hurdles for employees.

Conclusion

Amazon’s back-to-office policy shift has stirred conversations within the tech industry, raising questions about the balance between in-office collaboration and remote work flexibility. Companies will need to navigate these challenges to create work environments that cater to the needs of their employees while driving innovation and productivity.

Despite Amazon’s decision, the future of work arrangements in the tech industry still remains dynamic. It is likely that companies will continue to adopt a hybrid approach, offering a blend of in-office and remote workdays to cater to employee preferences and changing work norms. This flexibility could become a key differentiator for tech firms in attracting and retaining top talent.

To continue to remain competitive in the war for talent, companies can optimize their employee benefits to foster a better and more inclusive work environment. Pacific Prime is an award-winning global insurance broker and employee benefits specialist with over 20 years of experience in the industry. Our experts are adept at simplifying the complex insurance process to help your employee benefits package remain competitive in your industry.

Get in touch with Pacific Prime CXA to know more.

Content Creator at Pacific Prime

Vista is a content creator at Pacific Prime. With over 8 years of writing experience for online platforms on various topics such as luxury lifestyle and digital entertainment. He enjoys diving into complex and otherwise confusing topics, and creating easy-to-understand content for the readers to help them navigate through the topic – something that’s perfectly aligned with Pacific Prime’s motto of ‘simplifying insurance’.

Born and raised in the cultural melting pot that is Hong Kong, and having studied at an international school, Vista has developed a multicultural perspective that he uses in his writing and strives to connect to people of different backgrounds.

In his free time, Vista enjoys immersing himself in different worlds, from video games to light novels and movies. His hobbies help him expand his writing style by putting himself in the point-of-view of different people and characters.

Deciding between leasing and financing a car is a common dilemma for many prospective car owners. This decision carries significant financial implications and can also reflect personal lifestyle choices. Whether you prioritize having the latest model or prefer the long-term benefits of ownership, you want to weigh each option’s pros and cons. Moreover, your choice can affect your insurance premiums and coverage needs, making it essential to consider all aspects before committing.

Pros and Cons of Leasing

Leasing a car offers several advantages, making it an attractive option for specific demographics:

Access to Better Quality Vehicles: Leasing allows you to drive newer, higher-end models that might be out of reach if you were to finance or buy outright. Leasing allows you to enjoy the latest technology, safety features, and luxury without the higher price tag of ownership.

Lower Monthly Expenses: Monthly lease payments are typically lower than loan payments for financing the same vehicle. This can free up cash for other expenses or investments, making it easier to manage your monthly budget.

Minimal Maintenance Costs: A lease typically runs for three years, and the car is often covered under the manufacturer’s warranty for the entire term. The warranty can significantly reduce out-of-pocket expenses for repairs and maintenance.

Flexibility: Leasing allows you to drive a new car every few years. If you enjoy having the latest model or if your needs change frequently, leasing offers the flexibility to switch vehicles regularly.

However, leasing also comes with its downsides:

Mileage Limits: Most leases have strict mileage limits, typically around 10,000 to 15,000 miles per year. Exceeding these limits can result in costly penalties, making leasing less suitable for those with long commutes or frequent road trips.

Costs for Excess Wear and Tear: Leased vehicles must be returned in good condition. If the car shows excessive wear and tear, you may be charged additional fees at the end of the lease.

No Ownership: When you lease a car, you’re essentially renting it. You don’t build any equity in the vehicle, and at the end of the lease, you acquire no assets to show for your payments.

Higher Long-Term Costs: While lease payments are lower, they don’t contribute to ownership. Over the long term, continuously leasing vehicles can be more expensive than financing and owning a car outright.

Pros and Cons of Financing a Car

On the other hand, financing a car offers distinct benefits:

No Mileage Limits: When you finance a car, you own it, so there are no restrictions on how much you can drive. This freedom is ideal for those with longer commutes or a love for road trips.

Ownership and Building Equity: With each payment, you build equity in the vehicle. Once the loan is paid off, you own the car outright, and it becomes a valuable asset that you can sell or trade in when purchasing a new vehicle.

Customization Freedom: Financing a car gives you the freedom to customize your vehicle to your liking. Whether you upgrade the sound system, change the paint color, or add performance enhancements, you can modify the car without worrying about lease restrictions.

Potential Long-Term Savings: While monthly payments might be higher initially, financing can be more cost-effective in the long run. Once the loan is paid off, you’ll no longer have monthly payments, allowing you to save or invest that money elsewhere.

However, financing also has its drawbacks:

Higher Monthly Payments: Monthly payments for a car loan are usually higher than lease payments. The payments can strain your budget, especially when financing a more expensive vehicle.

Maintenance Costs Over Time: Maintenance and repair costs will likely increase as the car ages. Unlike a lease, which allows you to switch to a new vehicle more easily, financing means you’ll be responsible for these costs as the vehicle ages.

Risk of Negative Equity: When financing, you risk becoming “upside down” on your loan, meaning you owe more on the car than it’s worth. This can happen if the car depreciates faster than you pay off the loan, making it difficult to sell or trade in without incurring a loss.

Long-Term Financial Commitment: Financing a car involves a longer-term financial commitment, typically 3 to 7 years. If your financial situation changes or you want to switch vehicles, you may be stuck with a loan balance that needs to be paid off first.

Demographics Best Suited for Leasing

Leasing is often the best option for younger professionals in their 20s to early 40s who have a steady income and enjoy driving new cars. It’s also well-suited for urban dwellers living in cities who drive less and prefer the convenience and status of a newer model. Additionally, leasing can be a good fit for individuals with a lifestyle preference for switching cars frequently and who may use the car for business, benefiting from tax advantages.

Demographics Best Suited for Financing

Financing for a car typically appeals to a few specific groups. Firstly, it’s popular among families or individuals in their 30s to 50s who plan to keep the car long-term and build equity. Secondly, it’s a good option for rural or suburban residents who drive longer distances and need the flexibility of no mileage limits. Lastly, financing is also suitable for those with a lifestyle preference, such as drivers who prioritize long-term savings, want to customize their car or plan to keep it beyond the loan term.

Discover the Best Option for Your Car

Before deciding whether to lease or finance a car, assess your driving habits, financial situation, and long-term goals. Contact your local insurance agent for personalized advice and explore insurance options for your needs. Check out our additional resources for more tools to calculate the cost-effectiveness of leasing versus financing.

Setting up or running the small business of your dreams? Reduce your risks with these 13 retail store safety tips:

Step up your security. Minimize crime with security cameras, ample exterior lighting, and alarm systems. Ensure your security cameras cover key entrances and blind spots and invest in quality equipment. Teach team members how to turn alarms on and off. If an employee leaves your company, promptly change your alarm codes and passwords.

Think like a thief. Pretend you’re an intruder. What valuables can you easily spot from outside? What would you take? How would you get away with it? Putting yourself in a robber’s shoes can help you make proactive adjustments and prevent crime.

Drop off deposits. How much cash should you keep in your register? Choose a small amount you can still conduct business with and deposit the rest. In the event of a robbery, there will be less available to take. Additionally, avoid being too predictable by taking different routes to the bank.

Set out signs. If an area is under construction or out of order, note these hazards with clear signage. It’s also important to set out cones or wet floor signs when water is tracked inside or if something is leaking. Encourage your team members to be proactive about cleaning hazards and marking them.

Clear the clutter. If a customer falls and gets injured at your business, you could face expensive legal action. Avoid the risk by doing frequent decluttering sessions and minimizing tripping hazards on the floor and in high-traffic areas.

Be aware of your surroundings. Visibility helps make your retail store safer. When you’re in the store, you should be able to see out, and passersby should be able to see in. This way, your employees will see if someone dangerous is approaching. Additionally, onlookers will see if something dangerous, like a robbery, is happening inside and can call for help.

Add lighting. Eliminate any dark areas in your store and keep extra light bulbs easily accessible in a low bin or cabinet.

Add fire extinguishers. Every building should have a fire extinguisher on each floor. Get them inspected and tagged annually and give employees a refresher on how to use them.

Report potholes in your parking lot. Large cracks or craters could cause bodily harm or damage to vehicles. Contact your county, contractor, or the property owner to take care of them promptly.

Carefully screen candidates. Before you hire new team members, check their backgrounds. Meet them in person or talk to them on the phone to help verify their reputability.

Train your talent. Training is one of the most essential parts of hiring. Conduct extensive training for anything that’s part of a team member’s job description, as well as other functions of your business they may need to know. The better an employee is trained, the safer and more equipped they’ll be to navigate the job.

Be prepared for disaster. The best businesses are prepared for disasters and unexpected closures. Since you never know when one could strike, it’s crucial to be proactive with a disaster preparedness plan that includes steps for closing, reopening, and contacting your team and customers.

Invest in insurance. As a small business owner, you have enough things on your mind. Insurance shouldn’t be one of them. Get commercial coverage you can count on, like liability, workers compensation, or umbrella policies.

Could your retail store be more secure? Let our experts be the judge. Talk to a local, independent agent today.

This content was developed for general informational purposes only. While we strive to keep the information relevant and up to date, we make no guarantees or warranties regarding the completeness, accuracy, or reliability of the information, products, services, or graphics contained within the blog. The blog content is not intended to serve as professional or expert advice for your insurance needs. Contact your local, independent insurance agent for coverage advice and policy services.

Note: This guest post is by Frederick “Beau” Kron, an Independent Adjuster, Trainer, Appraiser & Umpire. He has written this post as an Independent Adjuster and not on behalf of the IAUA. Opinions expressed are solely his own and are not meant to express the views or opinions of the IAUA.

This year, a record-tying three hurricanes—Debby, Helene, and Milton—have made landfall in Florida. According to meteorologist Phil Klotzbach, this has only happened five other times in over 150 years, most recently in 2005. Previous occurrences were in 2004, 1964, 1886, and 1871. No season on record has seen more than three hurricanes make landfall in Florida.

For those of us in the industry back in 2004, you might remember grouping Hurricane Ivan with “The 4 of ’04.” Even though it impacted Florida, Ivan technically made landfall in Alabama, just west of the Alabama-Florida border.

In the wake of Hurricane Milton’s recent impact on Florida, a crucial question has emerged for property owners: When a tornado occurs during a hurricane but beyond the boundaries of hurricane-force winds, which insurance deductible applies?

The Milton Effect: A Tornado Outbreak

The National Oceanic and Atmospheric Administration Storm Prediction Center reported 38 preliminary eyewitness accounts of tornadoes during Hurricane Milton – a staggering number considering Florida’s average of 50 tornadoes in an entire year.

This deductible issue is particularly relevant for Palm Beach Gardens, an area that, despite being well outside of the hurricane-force wind path, experienced significant tornado damage — including an industrial dumpster landing on a residential roof.

The questions swirling around which deductible should be applied highlight the importance of understanding your policy’s definitions.

Dumpster on Palm Beach Gardens Home

Hurricane Deductible Confusion

Most homeowners policies include a hurricane deductible, typically higher than the standard wind or All Other Peril deductible. But when does this hurricane deductible come into play, especially in cases of tornado damage far away from the hurricane-force winds?

Let’s examine a sample AAA HO3 policy (FL 1000 1007) to shed light on this issue. This policy has a Hurricane Deductible:

SECTION 1 – HOMEOWNERS COVERAGES

PART I – PROPERTY COVERAGES

***

CONDITIONS – PART I

***

Hurricane Deductible

***

The hurricane deductible stated on the declarations page applies for loss or damage to covered property caused by all hurricane windstorms. A hurricane percentage deductible is determined by applying the percentage stated on the declarations page for hurricane to the COVERAGE A – DWELLING limit of liability at the time of the loss, but shall not be less than $500.

Deciphering Policy Definitions

The key to understanding whether this deductible applies is in the policy DEFINITIONS section, where terms in bold within the policy are explicitly defined. In this AAA policy, we find:

DEFINITIONS

***

Hurricane – means a storm system that has been declared to be a hurricane by the National Hurricane Center of the National Weather Service. The duration of the hurricane includes the time period, in Florida:

a. beginning at the time a hurricane watch or hurricane warning is issued for any part of Florida by the National Hurricane Center of the National Weather Service;

b. continuing for the time period during which the hurricane conditions exist anywhere in Florida; and

c. ending 72 hours following the termination of the last hurricane watch or hurricane warning issued for any part of Florida by the National Hurricane Center of the National Weather Service.

***

Hurricane windstorm – means wind, wind gusts, hail, rain, tornadoes, or cyclones caused by or resulting from a hurricane which results in direct physical loss or damage to property.

*emphasis added

The Conclusion

Based on the definitions in this particular policy, it is specifically stated that tornadoes occurring during a hurricane are considered part of the “hurricane windstorm.” This means that even if a tornado causes damage in an area with otherwise mild winds during the hurricane, the hurricane deductible would still apply. Your policy might be different.

Almost ten years ago, in Storm-Induced Tornado Damage, the Merlin Law Blog discussed a similar case where the lower courts deemed the State Farm policy language to be ambiguous. Even though the appeals court ultimately sided with the insurance company, the language in many policies has since been expanded for clarification, as in this AAA policy.

Key Takeaways for Property Owners

Review Your Policy: Carefully read your insurance policy, paying close attention to definitions and deductible clauses.

Understand the Definitions: Pay attention to how your policy defines terms like “hurricane,” “hurricane deductible,” “hurricane loss,” and “hurricane windstorm.” These definitions can significantly impact which deductible applies.

Document Damages: In the event of a loss, thoroughly document all damages, regardless of whether they seem hurricane or tornado-related. Damages caused by tornadoes are not always obvious and can be subtle but significant.

As we navigate the complexities of severe weather events, understanding your insurance policy becomes increasingly crucial. Stay informed with resources like Twelve Tips for Making a Claim for Tornado Damage to Your Property on Your Homeowner’s Insurance Policy, but don’t hesitate to seek clarification on your coverage from a professional.

Disclaimer: This blog post is for informational purposes only and should not be considered legal advice. Always consult with a licensed insurance professional or attorney for guidance on your specific situation.

All businesses rely on their employees to work together and succeed when it comes to achieving shared goals. In order for your staff to feel secure in their position, creating access to health benefits can be a supportive move.

There are many reasons why you should invest in small business group health insurance. A key factor is that employee access to healthcare actually increases productivity and engagement. Studies show that adding in health benefits for employees helps increase productivity by 5%.

A recent survey found that 90% of respondents said healthcare is a very important employee benefit. As this can be provided through group health insurance, it’s a helpful asset that employees can use to access medical appointments as required.

Contents

What is small business group health insurance?

How does small business group health insurance work?

5 major benefits of small business group health insurance.

Support employees with GasanMamo’s small business group health insurance.

What is small business group health insurance?

Small business group health insurance does not differ to a significant extent to large business group health insurance. However, partnering with an experienced business insurance provider ensures that the package you provide suits your individual business needs and the health concerns of your employees.

Group health insurance requirementscover the cost of medical expenses for medical investigations or treatment of an acute medical condition. This means your employees would be covered if they have a disease, illness or injury that is likely to quickly respond to treatment.

How does small business group health insurance work?

A group health insurance policy provides employees with access to healthcare on a risk pooling basis. This type of employee health insurance can be offered at a lower premium rate as the risk levels of employees are spread across all members.

Risk pooling generally lowers policy costing as group members carry the level of risk equally between them, compared to individual policies for employees and their families. This would increase costs as each policy would have to be created, assessed and managed on a case-by-case basis.

5 major benefits of small business group health insurance

Whether you want to keep valued employees within your business or simply care for your staff and their families, there are lots of advantages to small business group health insurance.

Employee loyalty

When you offer your employees the ability to access private medical and healthcare appointments, this naturally creates a sense of loyalty and belonging. New research suggests that companies with highly engaged employees are 21% more profitable and small business group health insurance can support this.

Talent retention

Attracting and retaining the right talent for your business can be a challenge in today’s fluctuating employment market. However, offering group health insurance benefits encourages your new hire to commit for longer. In fact, employees are 26% more likely than before 2020 to accept a new role because of a health benefit offering.

Absence reduction

If your employees gain access to timely medical appointments, appropriate mental health support and effective treatment plans, there is evidence that shows this reduces the amount of sick days employees take. This is because prevention is the key, meaning that employees can resolve any issues before they become more serious and impact their time at work.

Mental health support

The ability to check in with mental health support services for employees helps to boost levels of work satisfaction. Your staff can talk through any stresses that may affect their concentration and productivity at work, so they feel more equipped to achieve goals.

Enhanced productivity

Employee motivation can be a complex area to navigate for businesses. There is a combination of factors at play, such as goal orientation and workplace engagement. However, one aspect that many business leaders are clear about is that offering employees benefits they can’t find outside of work supports increased motivation levels.

If employees are able to focus and are committed to achieving targets at work, then this helps to increase productivity and creates efficiencies across the organisation.

Support employees with GasanMamo’s small business group health insurance

We underwrite and manage the following group health insurance plans:

Vital Plan

This offers limited insurance cover for in-patient and day-patient medical treatment in hospitals/clinics worldwide, excluding the USA and Canada. Available with additional benefits for outpatients, such as GP charge cover or diagnostic tests and medical procedures.

Key Plan

A more comprehensive plan which offers a full refund of fair and reasonable fees for in-patient and day-patient treatment in participating hospitals and clinics in Malta.

Limited cover is available up to the limits of the Vital Plan for treatment received worldwide, excluding the USA and Canada. The Key Plan also comes with out-patient benefits similar to the Vital Plan and International Plan.

International Plan

Our most comprehensive plan offers full refund of fair and reasonable fees for in-patient and day-patient treatment in Malta and anywhere in the world except the USA and Canada. Direct settlement of your in-patient and day-patient bills is possible with participating hospitals and clinics.

The plan covers outpatient benefits which include cover for GP charges, prescribed drugs, specialist consultation fees, alternative therapy, diagnostic procedures, and medical emergency dental care.

At GasanMamo, we like to help you prioritise your staff. Our health insurance policies are truly adaptable and deliver exclusive medical and health benefits. We support you with everything from policy initiation all the way to claims processing.

Interested in learning more or receiving a quote?

Visit our Group Health Insurance page or reach out to us by clicking Quote.

Virtual reality, or VR for short, may have some limited applications outside of video games and entertainment, but major US insurer Allstate Insurance Company believes there is potential in the technology for use in the insurance industry. Last week you were reading Swiss Re Exec On Whether Industry Is Making Real Progress. This week we’re bringing you:

Some customers can’t get no satisfaction with insurance apps

The streamlined user experience, seamless customer support and improved navigation that was supposed to define the digital transformation of the property/casualty insurance industry — and improve customer satisfaction — has been overpowered by rising rates, according to the J.D. Power 2022 U.S. Insurance Digital Experience Study released Tuesday.

The study showed that overall customer satisfaction with the property/casualty insurer digital shopping experience is just 499 on a 1,000-point scale, down 16 points from a year ago. This, despite significant investments in customer-facing websites and mobile apps.

“Although insurers keep upping the ante on technology, improvements are being offset by frustration among customers who are going online to shop for a better rate — and not finding one,” Robert M. Lajdziak, director of insurance intelligence at J.D. Power, said in a statement. “We’re also seeing a clear trend in which more than half of digital insurance shoppers are choosing not to use digital tools or educational resources to help them through the shopping process. This further exacerbates the decline in customer satisfaction.”

Read more in-depth here.

Cyber Insurance Premiums Up 27.5% to Lead All Lines in Q1: CIAB

According to The Council of Insurance Agents & Brokers’ (CIAB) Commercial Property/Casualty Market Index, capacity for cyber insurance may be decreasing while demand is increasing, which could have driven cyber premium price increases of an average 27.5% during the first three months of 2022.

Nearly 80% of respondents said capacity decreased during Q1, and more than 30% said the decrease was “significant.” Meanwhile, 90% of survey takers said there was an increase in demand for cyber insurance due to an “increased general awareness of the exposure faced by all individuals and organizations on a global basis without borders or regard for size, score or industry,” CIAB quoted one respondent.

Results from the survey indicated carriers are also requiring more from insureds to obtain cyber coverage. Many insurers require at least multifactor authentication or the potential policyholder is deemed “virtually uninsurable” and a quote is refused, CIAB reported. Agents and brokers also said carriers are requiring stronger passwords, third-part vendor management, an incident response plan, training of employees on phishing, penetration testing, system backups, and endpoint detection. Carriers are providing access to tools, assessments, consultations, and software to meet the requirements, respondents said.

Read more in-depth here.

Allstate files patent application for “insurance VR simulator”

Virtual reality, or VR for short, may have some limited applications outside of video games and entertainment, but major US insurer Allstate Insurance Company believes there is potential in the technology for use in the insurance industry.

A patent application assigned to Allstate was recently uncovered on the US Patent and Trademark Office (USPTO) website. Filed on November 12, 2021, the patent presents the idea of using VR in insurance.

NewsRx first broke news on the patent filing. The inventors who filed the patent believe that VR could ultimately help both consumers and insurers.

“Selecting an appropriate level of insurance is a challenge for most insurance customers,” the inventors said under the background information of the patent. “It can be difficult to gauge what kinds of liability coverage, deductible levels, and other options a particular user may wish to have, and many users end up selecting coverage that is either too much coverage or not enough coverage. There remains an ever-present need to help insurance customers make better-informed decisions when selecting their insurance.”

Read more in-depth here.

Finding highly affordable leads to keep sales coming in

At iLeads, we have many great solutions for insurance agents at a low cost. If you’d like to see how we can help you bring in consistent sales for a great price, give us a call at (877) 245-3237!

We’re free and are taking phone-calls from 7AM to 5PM PST, Monday through Friday.