As winter approaches, builders and contractors face unique challenges regarding construction sites. The cold temperatures, snow, and ice can put your project at risk. However, with the right planning and insurance, you can protect your investment and keep your construction site running smoothly. Let’s discuss essential winter preparations for construction sites, focusing on the importance of Builders Risk Insurance.

wooden frame for a building in snow

Winterizing Your Construction Site

Before the winter chill sets in, it’s essential to winterize your construction site to minimize potential risks and ensure the safety of your project. Here are some key steps to take:

Protecting Equipment: Cold temperatures can have a negative impact on machinery and equipment. Make sure to store them in a sheltered area or use weatherproof covers. It’s also a good idea to keep your equipment well-lubricated to prevent freezing.

Snow Removal Plan: Set up a snow removal plan to keep your site accessible. Regularly clear snow and ice from pathways, parking areas, and entrances. This not only ensures safety but also keeps your project on schedule.

Heating Systems: If your project requires on-site offices or trailers, ensure they have proper heating systems. These should be regularly maintained and inspected for safety.

Materials Storage: Store materials indoors or under a protective cover to prevent damage from moisture and freezing temperatures. This helps avoid costly material replacement.

Insulate Pipes: Insulate water and plumbing systems to prevent freezing and potential damage. Burst pipes can be a significant setback for any construction project.

Builders Risk Insurance: Your Winter Safety Net

While these winter preparation steps are crucial, unforeseen events can still happen. This is where Builders Risk Insurance comes into play. Builders Risk Insurance is specifically designed to protect construction projects from risks like theft, vandalism, fire, and natural disasters, including winter-related issues.

Winter preparations are a crucial part of construction site management, and Builders Risk Insurance plays a significant role in safeguarding your project. By taking steps to protect your equipment, materials, and site, you can minimize risks.

Bankers Insurance Group is here to provide the coverage you need to ensure a successful winter construction season. Get a quote today. Our team is ready to assist you in finding the perfect Builders Risk Insurance coverage for your needs. Stay safe this winter season!

Read more: Recipient of 2022 5-star Construction Excellence Award from Insurance Business America Magazine

In Michigan, a No-Fault lost wages claim from a car accident refers to the compensation you may be entitled to (85% of a person’s wages, tax-free, for up to three years from the date of the crash – regardless of fault) for the income you lost due to injuries sustained which prevent you from returning to work.

For crash victims and their families who are already worried about recovering from injuries, getting necessary medical care and continuing to pay bills, this No-Fault benefit is one of the most important legal rights that people have under our state’s unique auto No Fault law.

What are lost wages from a car accident in Michigan?

Under the Michigan No-Fault Law, a lost wages claim from a car accident provides reimbursement to crash victims for 85% of the income they would have earned during the first three years after the crash had their crash-related injuries not disabled them from returning to work. (MCL 500.3107(1)(b))

How to claim lost wages from a car accident in Michigan

To make a lost wages claim from a car accident in Michigan, a victim must: file an application for No-Fault benefits with the auto insurance company; provide proof of income lost from not returning to work; provide a work disability certificate from the doctor; and provide wage verification from his or her employer.

Any or all of the following documents can be used to provide “reasonable proof” of a victim’s income for purposes of claiming these No-Fault benefits:

A “Michigan Motor Vehicle No-Fault Insurance Law Wage, Salary and Benefits Verification” form completed by the victim’s employer.

A copy of the victim’s pay stubs for the two months prior to the crash.

A copy of the victim’s most recent W2, i.e., the Internal Revenue Service’s “Form W-2 Wage and Tax Statement.”

To document that a doctor has deemed a crash victim disabled from returning to work, victims can use our “Work Disability Certificate” form.

The No-Fault law in Michigan merely requires “reasonable proof” be provided so a lost wages claim from a car accident can be paid in a prompt and expeditious manner. (MCL 500.3142(2))

Are these No-Fault benefits available if someone was temporarily unemployed?

Yes. For a Michigan crash victim who was “temporarily unemployed” — or even who was working reduced hours — at the time of a crash, his or her lost wages claim from a car accident shall be based on earned income for the last month employed full time preceding the crash. (MCL 500.3107a)

That means people who can show they are actively looking for employment when they are injured in a crash can still recover income loss from work from their No-Fault insurance companies.

How to claim lost wages from a car accident in Michigan?

In Michigan, to make a claim for lost wages after a car accident a person must have suffered an injury, i.e., an “accidental bodily injury,” resulting from a crash. (MCL 500.3105(1)) Additionally, the injury must be the reason that the crash victim is unable to return to work.

Can I claim lost wages for a car accident without injury in Michigan?

In Michigan, you cannot make a claim for lost wages if you have not suffered an injury in a car accident that prevents you from working. Michigan No-Fault benefits, including reimbursement for income losses, are payable only if a person has suffered an “accidental bodily injury” from a crash.

Calculating A Claim

Under Michigan’s auto No-Fault insurance law, your lost wages claim from a car accident will be 85% of the monthly income you would’ve earned if your injuries hadn’t disabled you from working. However, your payment is subject to a monthly maximum. The 15% reduction is because these No-Fault benefits are not taxable income.

How much can a person receive in a claim?

If a person suffers injuries that prevent him or her from returning to work, then a Michigan No-Fault lost wages claim from a car accident will pay up to 85% of the “income from work” the “injured person” would have earned “if he or she had not been injured.” (MCL 500.3107(1)(b))

However, these benefits are capped at a monthly “maximum” amount (see below) that’s “adjusted annually to reflect changes in the cost of living,” but a “change in the maximum shall apply only to benefits arising out of accidents occurring subsequent to the date of change in the maximum.” (MCL 500.3107(1)(b))

What is the Michigan No-Fault wage loss maximum?

The Michigan No-Fault wage loss benefits maximum is $7,014 per month for the period of October 1, 2024, through September 30, 2025.

Previously, it was $6,811 per month for the period of October 1, 2023, through September 30, 2024. Before that, it was $6,615 per month for the period of October 1, 2022, through September 30, 2023. It was $6,065 per month for the period of October 1, 2021, through September 30, 2022. It was $5,755 per month for the period of October 1, 2020, through September 30, 2021, and it was $5,718 per month for October 1, 2019, through September 30, 2020.

The monthly maximum that applies to a person’s claim for benefits is the monthly maximum that was in effect at the time that his or her motor vehicle crash occurred.

Can I get lost wages claim from a car accident in Michigan beyond the limits in the No-Fault law?

In Michigan, to obtain a lost wages claim from a car accident that exceeds the monthly maximum amount or the 3-year limit – and/or future income loss from work and future economic loss – a victim will need to file a third-party tort lawsuit against the at-fault driver for “excess” and/or “future” income loss from work. (MCL 500.3135(3)(c)). A lawyer can then sue on your behalf for all future economic loss not paid by No-Fault insurance, including income lost from work in excess of the statutory monthly maximum, in a tort (or injury) lawsuit against the negligent, at-fault driver who caused the crash.

Who pays for these No-Fault benefits after a crash?

Michigan No-Fault lost wages claims from a car accident are paid by a person’s auto insurance company (or the auto insurance company that is determined to be liable under the No-Fault “priority” rules). (MCL 500.3105(1))

Can I claim the No-Fault benefits if I caused the crash?

Yes. Claims are paid “without regard to fault,” i.e., even if the injured person who is seeking these No-Fault benefits was at-fault in causing the crash. (MCL 500.3105(2))

However, this means you will be limited to only recovering these benefits from your own No-Fault insurance company. You cannot sue yourself in tort for your injuries and pain and suffering and future and excess economic loss if you caused the crash.

How long can a crash victim receive these No-Fault benefits?

A claim will be paid “during the first 3 years after the date of the accident.” (MCL 500.3107(1)(b))

When will I receive a check for my claim?

The auto insurance company is supposed to pay you “within 30 days” of receiving “reasonable proof” of your “loss of income from work an injured person would have performed during the first 3 years after the date of the crash if he or she had not been injured.” (MCL 500.3142(2); 500.3107(1)(b))

If the auto insurance company has received “reasonable proof” of your lost wages claim from a car accident in Michigan and fails to pay within 30 days, then your benefits are “overdue.”

Our auto crash attorneys strongly recommend calling your insurance adjuster after each submittal to confirm receipt and to inquire about whether any additional documentation is needed from you. Once you receive confirmation that your wage and salary verification form and whatever additional information has been received by your claims adjuster, and that your claims adjuster has told you that the information is sufficient and there is no additional information to constitute reasonable proof, document that as well in a separate letter or email so that the 30 days begins to run.

You do not need to hire a lawyer to receive lost wages after a crash for lost hours or other Michigan No-Fault benefits (and you should run from any lawyer who tells you that you do). That said, we always recommend talking to an experienced auto No-Fault lawyer to make sure you are receiving everything you should be and you are protecting your legal rights. The initial phone call and consultation is always free of charge.

I wrote “supposed to pay” above for a reason. From experience, unfortunately, the 30-day rule is something that far too many claims adjusters ignore. Sadly, for too many innocent and injured people waiting for compensation, you are just one more file. A claims adjuster can easily have two or three hundred claims open at a time. In a state like Michigan that does not have insurance bad faith laws or punitive damages to stop adjusters from ignoring claims, it is often very hard to get a claims adjuster to make prompt payments. That leaves people with the unenviable choice of continuing to be ignored or hiring a lawyer to sue for incurred and outstanding No-Fault benefits and income loss from work. Even when a person has hired a lawyer and started a lawsuit for outstanding benefits, you will likely only recover penalty interest and attorney fees by taking the case to judgment or verdict, so there is often no real deterrent to force adjusters to pay outstanding claims promptly.

Can I claim these No-Fault benefits on my taxes?

No you can’t claim lost wages from a car accident on your taxes in Michigan. These No-Fault benefits that victims receive from their auto insurance company are not taxable income” under Michigan law. Because they are not taxable, benefits are reduced 15%, leaving the victim a payment equal to 85% of their wages. (MCL 500.3107(1)(b))

However, if as part of a third-party tort lawsuit a crash victim seeks “excess” income loss benefits from work beyond the monthly and/or 3-year limits – or future income loss – then any such recovery will be treated as income that will be taxed. Importantly, taxes should include social security and Medicare taxes.

Were you injured in a car accident in Michigan and need help with your No-Fault lost wages claim? Call now for a free consultation!

If you have been injured in a crash and you need help with your Michigan No-Fault lost wages claim from a car accident, call now (800) 968-1001 for a free consultation with one of our experienced car accident lawyers. There is no cost or obligation. You can also visit our contact page or use the chat feature on our website.

Michigan Auto Law is Michigan’s largest and most successful law firm that specializes exclusively in helping people who have been injured in motor vehicle crashes.

Our secret? Our attorneys deliberately handle fewer cases than other personal injury law firms. This allows us to focus more time and attention on our cases.

Unlike other law firms, our attorneys are never too busy to promptly return phone calls and answer questions.

We have more than 2,000 5-Star reviews that reflect this care and attention to detail.

More importantly, this client-focused approach leads to better and faster settlements for our clients. Michigan Auto Law has recovered more million-dollar settlements and trial verdicts for motor vehicle crashes than any other lawyer or law firm in Michigan. We’ve also recovered the highest ever reported truck crash and car crash settlement in the state.

Call now so we can start making a real difference for you.

Did you know that Boshers Insurance do more than provide high-quality insurance for Holiday Home owners? We also support The 2 Minute Foundation, a charity whose vision is to clean up the planet, 2 minutes at a time. So, if you have ever despaired at the state of many of our beaches, there is hope!

How it Started

The 2 Minute Foundation has been up and running for over a decade. It started with Martin Dorey putting a post out on Twitter saying he was going to do a 2-minute beach clean and who was in? The result was it became a massive social media movement, with hundreds of thousands of people posting their 2-minute beach cleans on The Two Minute Foundation’s social media channels!

What is the Problem?

If people and corporations do not change their behaviour, scientists calculate by 2050 between 850-950 million tonnes of plastic will be in our oceans. That is the equivalent of 5 million Antarctic blue whales (the heaviest animal in the world).1

The increasing amount of plastic pollution has caused over 78% of marine mammals being at risk of accidental deaths. An example of this is marine mammals getting caught in fishing nets, which kills over 1,000,000 sea animals every year. In the UK alone, 700,000 plastic water bottles are littered every day, and these statistics are only the tip of the iceberg.2

What is the Solution?

If everyone in the UK was to pick up at least two pieces of litter, over 136 million pieces of litter would be removed from our coastlines, which is the basis for The 2 Minute Foundation’s mission and vision to clean up the planet, 2 minutes at a time.3

How the 2 Minute Foundation Makes a Difference

The 2 Minute Foundation is a charity that enables people to pick up litter. Wherever there’s a station, someone can use the equipment free of charge to collect plastics and other types of litter. People can borrow litter pickers and bags from stations in various locations, collect and tag the bags, recycle what they can, bin the rest, and return the pickers and bags.

Mobilising communities all around the UK; they started off with one or two litter picking stations and now have over 1,000 in the UK and Ireland.4 You can be out walking your dog, on a beach excursion for the day, or be more adventurous and take the litter picker out on a paddle board and collect from the sea. The Two Minute Foundation encourages people from all walks of life and in any location to be better stewards of the planet.

How Does Boshers Insurance Help?

As part of a collective of businesses which support The 2 Minute Foundation, Boshers are really proud to be part of the Foundation’s journey in cleaning up the planet.

We have been working alongside The 2 Minute Foundation since 2022, and are part of a host of companies supporting the Foundation’s work, including:

The National Lottery

Channel 4

Volkswagen

Dryrobe

LUSH Fresh Handmade Cosmetics

… and of course – Boshers Insurance.

It’s no one’s responsibility to pick litter up, which makes it everyone’s responsibility. That’s why the Boshers team are going to do a beach clean up in the very near future (follow us on Linked In, Facebook and Instagram to keep tabs on the Boshers Big Beach Clean!), and support The 2 Minute Foundation in every way we can.

If you’d like to get involved with cleaning up our planet – 2 minutes at a time – contact The 2 Minute Foundation via their website: https://2minute.org/

If you’d like to follow them on social media and post your own beach clean, please visit the social media links below.

To find out more about Boshers Insurance and our collaboration with The 2 Minute Foundation, our team are on standby to provide more information.

Or if you would like a new quote for your holiday home or holiday let insurance, please contact us today.

Quotes & Enquiries: 01237 429 444

Email: info@boshers.co.uk

1-3. The 2 Minute Foundation Fundraising Pack July 2024

https://2minute.org/About-Us

Boshers Ltd are authorised and regulated by the Financial Conduct Authority under register number 224623. Boshers Ltd are registered in England No. 02946794. Registered office: Affinity House, Bindon Road, Taunton, Somerset, TA2 6AA. Calls may be recorded for use in quality management, training and customer support.

Your host of the QuotersCast and licensed insurance agent Renee talks to Rick Elmore who is the Founder of SimplyNoted.com.

Elmore is a former NFL football player turned medical device salesperson turned expert marketer and now industry changing tech mogul. Discover what this former linebacker is doing with his determination and grit now!

SimplyNoted writes and sends Real Handwritten Notes to your clients, customers and prospects to increase your sales and open rate exponentially. Discover what this innovative robotics technology is doing to help service based professionals increase their business today!

RENEE HOST OF QUOTERSCAST: Alright, my guest today is Rick Elmore, who is the CEO and founder of simply noted. He’s also a marketing expert, and you were a top salesperson at several medical equipment companies, and this is a big twist for a really life at 65. You spent three years in the NFL. Right, I think that’s awesome. You’re… That’s excellent, thank you. Sure. Yeah, I’m looking forward to this because this… Your technology and the company that you’ve built directly affects someone like me, and I just think you’ve got such an interesting background experience, so can you give us a little bit… I mean, you’ve only been in business since… Was it 2017? And you’re now already about 2 million annually, in revenue. That’s pretty amazing. Yeah, that’s pretty amazing. You give us a little bit of background on how you came to this. And we’ll go from there.

RICK ELMORE OF SIMPLYNOTED: Great, well, thanks for holding me, like You send my backgrounds in athletes, football, the sport that I love with the University of Arizona, played for Mike’s tops in 2006, was really lucky and had a good career, there was drafted in genitalia, you got to spend a few years there in the belly, chopped am eventually like most, or you have to hang up the shoulder pads and cleans and get into the real world, so I got into that corporate medical device sales and marketing, first years, Rocky the year, basically just take everything that was good as an athlete, Harper severance, great, get knocked down nine times, get up 10, and just applied it to my corporate career. So the first year I was Rookie, next five years, I was either a top 1% or top five sales rep in my company, and again, it was just all efforts in 2017, I just could not Scratch, so I went back and did my MBA, I just… I knew there was something else out there for me, and in 2017, I had a full-time job, I had my first child that year, I did an Ironman, but even my program launch launched my first startup.

RE of SN: So yeah, 2017 was a wild year, but I was in the Marketing class and December, but here to my program, and at a marketing professor said that handwritten notes have a 99% open rate, and I just thought that was just an amazing statistic, since we live in a very digital, digital overload world, it’s just really hard to engage people, so I thought if I can send some handers with the 99% grade, and it has to make me more successful if I can get in front of my client 99% of the time. And the classmate of on myself, I got together, I worked with some technology at a China is just a pen plotter was a very bad technology and just tested it and tested it and tested it, we just had great results and partly rose in 2018, most simply noted, fast forward five years were the largest handwriting platform in the world, were the only cup in the role that’s truly better on handwriting, robotic mean by that we leverage no op to shelf solutions, everything that we build is custom to us. I never thought I’d do this, but we’re gonna have six patents on our technology, designed through utility, we have hundreds of thousands of users on our platform every single month, it’s grown tremendously about the same as easy, but it wasn’t…

RE of SN: It’s been a lot of less winters, I’ve gone into this, but I think the solution that we provide is solving a big problem in today’s digital and AI world, and that’s just the personal tangible touch where the mailbox is empty, where nobody is competing. And that handwritten note really stands up and that mailbox…

R of QC: Yeah, I totally agree. And being in the field that I’m in, I’ve written a lot of those myself, it takes a lot of time, and so I’d like to drill down a little bit on the actual technology, ’cause I really do think this is like what you’re doing, you’re taking like you say the human touch and you’re using technology to marry it. So number one, how much of the artificial intelligence play a role in this?

RE of SN: Well, I think that’s a very buzzword now since… What was it in November 22, when Open AI released chat spent the way that we’re leveraging it right now is just helping people kind of formulate and give them ideas on what they’re gonna say, so we’re actually launching that update on our website, but it’s been a week so you’re gonna belly go and say, Hey, help you it think you know to John or help me a congratulations, or selling your house or whatever. So that’s the only way that we’re leveraging right now, what we’re trying to do is help businesses either automate it, so it becomes predictable, a part of their sales or marketing plan, or scale it, if you wanna send one or two… We can help you do that, but we actually consult and say, Hey, if you can send one or two by yourself do it yourself, but we’re trying to build a platform to help companies automated or scale it.

R of QC: Okay, so you tend to prefer to work with agencies then and larger companies.

RE of SN: So… Sure. We’re not trying to monopolize the handwritten note market by any means, we’re just… We’re trying to develop a tool that businesses can leverage within their marketing or MarTech stack where they can know at a handwritten solution, just like they have a calling solution, an email solution, a CRM, we’re trying to be the handwritten solution that they can put her to

R of QC: Outright so I know it took a lot for you to invest in this financially, so what does it look like in terms of your team and the partners that you have to get this going off the ground side, you mentioned one partner, but you have a lot of investors have you used your own money… Is that

RE of SN: Zero? We’re completely customer-funded. Not no investors. Yeah, so when I started this company, I really wanted the proof, I wanna improve myself and when I could do it, but I don’t come from a background of money, I don’t ingroup with a silver spoon or go smoother, they call it. My parents were very supportive, but we didn’t have tons of money growing up, so I really didn’t have a lot of options, so another way for me to do this was to self-funded and how we funded it was just dealing what I was good at, I would go out, identify opportunities, show the client what we can do for them, solve a problem for them, and then we close and reinvest the proceeds back in the business.

R of WC: Okay, you’re a very fascinating character to me, because from your athletic background, a, you’ll give you this it up, I’ll tell you why, because you went from football into selling medical equipment and then now you help this handwritten is… There’s nothing like this out there. And so to start this up in the way that you did, and all the effort and time that went into it, there had to have been something in your thinking process that made you decide that this thing was gonna be the thing that you were gonna spend that much time and energy on, and I would love to hear what… What was the reasoning?

RE of SN: Exactly, so I grew up in the generation without technology, I didn’t get my first cell phone until I was almost 17 years old, and it was one of those brick toivonen when I was being recruited in high school, any coach… I think it was 29 or 30 division when football offers or scholarships, but the coaches that really set out to me with the ones that sent me hand-written up that show me that they invest some time into reaching out to me, I got tons of printed letters and postcards. And that was easy to do it. So anybody who sent me a handwritten note that immediately set up when I left the 49ers in 2012, carbo set me a hand-written up and he’s a head football coach in the NFL, and now he’s back in college, but that guys a person of influence and that impacted me so much. It literally made me a… No.

<—— Tech Problems – The Zoom Froze —->

R of QC: You were in the middle of telling us about your coach would send you the hand-written note, and I just wanted to make the point that you’re a tough guy and you come across really forthright, but clearly you have a huge heart, and that’s kind of what I wanted to highlight here and you live a great story.

RE of SN: Alright, so yeah, a handwritten notes, Why did it mean so much? And why they have impacted in my life so much, so there was a good story. Back in 2012, when I was playing for the San Francisco 49ers, I left the team after that season, we went to the NSC championship game and lost write for the Super Bowl. So it was a pretty awesome year, but when I left the team, coach harbor, a very influential leader, head coach in the NFL, he’s now back in the college ranks. You sent me a handwritten note, and when I was like 23, 24 at the time, and when I got that three or four weeks later after I left, I just… It impacted my life so much. It meant so much to me that he would sit down and take the time to do it. It’s actually a keepsake, literally, I kept it, it’s in my office on my shelf and I’m gonna be able to share that with my kids some day, so that’s what we’re to do at scale for companies, I think people want to do it. And the problem that we’re solving is that they don’t have time to do it, so now we’re creating a platform that helps them to do it.

RE of SN: Again, I’m not telling anybody You should send every single handwritten, you know that you ever do through our platform, but if you’re a business, if you like systems and processes, you have a CRM, you wanna stay consistent, you wanna make sure the grammar is right, you’re not having your assistant, and you don’t have to worry about the misspelling something or the grammar is not right, we’ve built the platform that helps you automated or scale it, so you… An automated birthday card, an anniversary card, is not a holiday cards, or just send out a thank you card, which is a big part of our business is the law of reciprocity is just building those relationships. And we all know how important relationships are in business, I can develop this business if it wasn’t for my relationships, I know almost every business out there wouldn’t have their business if they didn’t have loyal relationships, so it’s all about the relationship and a good… Simple Banking Up is a way to solidify a strong relationship with our clients…

R of QC: That’s great, and I know you have… You’re big on follow-up, so I’m assuming you might have a whole system and philosophy, that’s what I’m guessing. Do you

RE of SN: Mean for follow-up, it’s just based off of triggers, so say that you had somebody come and book a meeting with you, we can automate handwritten note to be sent out after that meeting is completed, or if somebody signed up for a quote, we can automate Hey, thank you for reaching out for a quote, we’re excited to work with you, we can automate sending that follow-up part, it’s really just based off of triggers that are happening within your company CRM or software, whatever you use, any time someone pays a bill, we can automate sending your card. Hey, thanks for paying your bill, so I really set up systems that help you automate your personal touch, but it really… It’s just as easy as sending an email, if you have a spreadsheet in Excel sheet by send it to us, it’s just like Nalanda were pugin a variables high first name, every car is completely custom to that individual, so it could be as easy as you want or as complicated as you want, we just have the software, the technology, the platform, the robots, all the milling equipment in-house, all the printers in-house, we’re a one-stop solution to make sending and scaling handwrite notes as easy as possible.

W of QC: Wow, that’s amazing. So do you, as a great sales person that you are… I’m thinking about some of the big old insurance companies with thousands of agents and a lot of the independent agencies, it just sounds like this is perfect because they have Salesforce and Zapier and all that kind of stuff, this sounds like the perfect service to sort of integrate with that, have you approached them, and if so, how did that get…

RE of SN: You tried so many times. Oh really? We have… I think we saw Farmers, I’m not sure, I don’t know who our insurances or maybe they do one of our things that we have, but I get a really crappy 5 cent post card for my birthday every year from them, and I’m like literally like, Why are you sending me this, why… This literally shows me that you put zero time and effort into this, and it’s just like, This is not gonna do anything from my relationship with your company, and I’ve tried… Literally, it’s all about dollars and cents. It doesn’t matter about relationships, brand recognition, loyalty, referrals, reviews, I’m just like… I literally don’t even look at it, I get it now, I just do a straight in the trash, I says like, This is the least amount of effort your company in a possibly done we run or on printing press in our warehouse. I know how easy it is to print out these postcards, I could print 11000 of them an hour, so it’s like… Anyways, we’ve tried… And I think what happens eventually, or these companies will come around when they start seeing their competitors use it and they start seeing the success they have, but there’s usually the smaller agencies that we work with, the ones that really understand the value of a referral, the ones that really understand the value of the lifetime value of a client, or the ones that are running in anywhere from 700 to 3000 booklets a portfolio, so it’s the big mega conglomerate, they don’t even in…

RE of SN: Give you a second, I’m just like, Alright, it’s fine. I know

R of QC: You’re right, there’s second 70 sea. One thing I notice when doing research on you, you mentioned I thought this was really important that you don’t like to overlook any small opportunity because you never know where it’s going to lead, and so that kind of every… So can you give us an example of a small… Look like a small opportunity on the surface that turned out to be something big.

RE of SN: So when I first started, I did every business networking event possible, I did the BIs, the Chamber of Commerce, the vestiges, the small, private… I did the, what do you call the speaking one, hematoma, Ter Toastmasters or… I’ve done them all, and none of them are really a good fit, but I was a young entrepreneur, just trying to get out there, meet people, be around people that are doing something similar to me, and I remember I did Van in my first year and my largest I got a referral from someone at B and I to somebody two years after I left, like, Hey, you should talk to this guy. And I spent year in the program and I really did nothing for my business, but I built relationships with in band I, and they connected me to somebody that ended up being a massive six-figure client for us, so you can’t discredit any effort whatsoever. You can’t leave any stone unturned, you can’t overlook any bad experience, you have to fix every experience, you can’t say though that guy is a bad customer, he’s not a good person, you have to obsess about that stuff, and that’s what I’ve done really well.

RE of SN: That’s simply not it. It’s like I just, I will go above and beyond, go a lot further than any of our… Now, that’s why I make Gonsalves incorporate in the corporate was willing to do a lot more than my competitors or the people that I worked with, and that’s what helped me set myself amongst the crowd, so we would do the same thing here. It’s more tremendously well. It’s very exhausting that I don’t know if I can do it, and I started when I was 29. So we booked a… I don’t know if I would start it the same way, I’m a lot smarter than I was when I was 20 years old. Well, yeah, absolutely. At that 100 client, it can be just as valuable. Is that 5000 client is just… You can’t overlook anybody.

R of QC: Wow, that’s a great attitude. So what is that? When you say you go above and beyond, can you give us examples of what it was

RE of SN: That… I think it’s pride. I think a lot of people get stuck and trying to make sure that they’re right or I’m right, versus the customer, I don’t care, I’ll step down my pride in it, even if they’re way wrong, I’m like, You know what, I totally understand. We’re so sorry and just move on because it’s not worth the drag dragged out an email battle, they go on and get their friends to write bad reviews, they write the bad reviews, it’s just people have to let go of their pride, they have to look other ego, a lot of people getting a running their own business because they wanna be their own boss, but even though my own boss, I’m still more in sales, and I would say at the beckoning call more people now, I used to just be having to service my clients. Now I have to service my vendors, my employees, or clients, or engineers or developers. So I think if there’s a lot of independent insurance or business owners out there, just get with making sure that your clients are happy, even if you have to swallow your pride a little bit, believe me, it’s gonna pay off.

RE of SN: A year from now, two years from now, because they know they’re wrong and you tell them that they’re right, they’ll come back, I will refer somebody because they know you’re somebody that’s willing to be flexible and work with them. That’s great. Yeah, excellent.

R of QC: So you are able to sell these notes and letters with him without envelopes, they’re very affordably, and after talking to you now for a few minutes, I’m assuming it’s gonna be on great paper and have a quality and blood stuff with the manufacturing and all equipment that you have… And the materials you need. How is that possible? Really to be that competitive.

RE of SN: So I mean, the first four years, it was really hard, it was really hard to not get too low on price because we needed the money that we got from selling… To reinvest back in the business, we’ve invested almost a million dollars now adjust into the development of our handwriting robots, and that’s all customer bondage, so that comes from sales, that’s not to account for a run or a fourth version of our website, probably spent near another million dollars just in software development, not including capital equipment, all the mailing equipment, the printers, which is another probably 60 or 70000, so at this point now where we’re at, now that we have all this stuff in-house and we can control our costs a lot better, we’re able to get a much better price on our service, so we’re still well below, it’s gonna cost for you to go to a store and buy a car and do it yourself, you go to the store and buying greeting cards to be four or five bucks, just the car plus postage, and a lot of our businesses that the volumes they’re doing it, they’re doing it for around a dollar a cart, plus post it or selling at…

RE of SN: Again, it’s real handwritten umbrella Rank card on a 120-pound car stock, which is thicker than a whole Mark card, and it’s automated at scale, you’re not gonna have Carpathians and you worries about an injury being delayed or stuff like that, and it really is a remarkable technology and that’s what we’re trying to do is get the word out there. There’s nothing else like it. Only came in the world that’s truly built in on handwriting robot, we built her handwriting engine, we can literally take your handwriting style, all the characteristics out of it, and truly is your hand writing to put words on paper to send to your clients. And that’s like when people grasp that and they’re like, Holy crap, it’s as easy as sending an email and I can use my hand writing with my customization Ary, and it’s automated, that’s when a light bulb started exploding and they get excited and then we can’t… They get in contact with us and we help them get going.

R of QC: Yeah. Wow, that is really remarkable. ’cause from watching the robot do its thing, I wouldn’t… It looks so real, but I had no idea that you… Nickerson is handwriting, so… Yeah, go ahead, please.

RE of SN: Yeah, when we mimic a person’s handwriting is not a simple hand write or a fun conversion, so I find when you’re creating a font online, so onshore created in the 90s for the internet, so they’re tiles or of files, truetype or open type on… We actually create something that’s completely different. It’s a handwriting style, so we will pull out all the unique characteristics within your handwriting, the spacing, which is called carinthia URS, which is how your letters naturally connect to each other, so some people will connect their toes or connect or end to them together, or to age or what do to ease look like next to each other. We program, I’ll pull out all that out, program in your handwriting style, and then we actually have an algorithm that takes your handwriting style and manipulate it as it writes it, so it doesn’t matter if you wrote a 1000 as right next to each other on our robot, not one single, Hey, we’ll let the same… It rotates it, that stretches it, it makes a bigger, smaller… There’s way too much stock put into this week freer on pens, we literally… Our pen run out so much, we had to create our own pens, the type of an duties in a pen.

RE of SN: The Weta ability of the ink was thought about, it’s called viscosity, so it actually smear is really good when you like You dumb and try to smear it, so this way too much thought that goes into a simple one, two… Or the hand-written note. But were… We believe so much in it, the problem that we’re solving, we believe that handwritten notes or handwrite Mall is gonna come back with mentioned, especially being in the digital world for the last 23 years, and now we’re going to the AI world, and we’re just a platform that’s ready to help people do it. Yeah, definitely. That’s what it sounds like.

R of QC: So you’re not worried about China copying you are you…

RE of SN: I don’t care, there’s… I think in the post office, there’s like 74 billion pieces of First Class Mail alone sent every year. I don’t even want 5% of that, but it would be a nightmare to manage. So we wanna work with clients that are good people that understand the value of the service, we’re not trying to monopolize anything, I’m happy just to get out there and work with great people and provide a great service.

R of QC: Okay, so you haven’t really thought of other applications for this then, in what ways… Well, I don’t know. Just listening to it. It’s so complex. I don’t know, I haven’t…

RE of SN: Well, there’s definitely another application for individuals with writing disabilities, we’ve talked to non-profits to help them use our systems to write. But that’s just a completely different conversation.

R of QC: I was just thinking even a book or a textbook to make it look like somebody had actually physically written it, and that might be something to get rid of e-books and maybe having an alternative, would that be cheaper than regular printing.

RE of SN: Alright, not it takes what are robot… About five minutes to write one hand-written note, and that’s about 100 words, so it writes as fast as a person… We can speak it up and they write it as fast as we want, since these are machines, but the faster you go, you suffer writing quality, so we wanna make sure it looks great, so the role just scale, we just have more Robots to the production line to help us turn orders faster versus turn the machines up in speed. Okay, alright.

R of QC: And maybe lastly, I’m just curious, have you tried to infiltrate for the football organizations and with this technology and…

RE of SN: We worked with the NCAA a little bit in the early days. It’s not really our niche, we wanna work with the service-based industries, real estate, mortgage insurance, non-profit where relationships matter, where the value of saying thank you is gonna impact their business for years to come, ’cause we all bring a business… I’m trying to shut down my turn rate ’cause we all know it cost more to your client then keep your clients happy and get referrals, so we’d like to focus on those industries that value relationships. Alright.

R of QC: Well, that’s great, I wish you much. Continued success. This has been an awesome interview. And you’re super impressive. Rick, thank you very much for being here.

RE of SN: Thanks for having me. Have a great day, see you.

Understanding the reasons behind a denied claim is only the first step in the labyrinthine journey towards resolution. Each path presents its own hurdles and opportunities, demanding a strategic approach and unwavering perseverance.

Delving into Policy Exclusions: Policy wordings, while seemingly innocuous, often hold the key to understanding exclusions. Hidden within the technical jargon lie limitations you might have overlooked. For instance, a seemingly comprehensive health insurance policy might exclude alternative therapies or experimental treatments. Familiarize yourself with these nuances, consulting with your agent or legal counsel if uncertainties arise. (Source: National Association of Insurance Commissioners, “Understanding Your Health Insurance Policy”)

Home Insurance

Building Your Case: A denied claim isn’t necessarily the final verdict. Gather any documentation that strengthens your narrative. Medical records, police reports, witness statements, and detailed photographic evidence can be crucial in substantiating your case. Remember, the more compelling your evidence, the more likely you are to persuade the adjuster of the legitimacy of your claim. (Source: Insurance Information Institute, “How to File an Insurance Claim”)

Navigating Appeals and External Reviews: If your initial appeal falls short, escalate the issue. Most insurance companies have internal appeals processes, typically involving a higher-level representative. Utilize this opportunity to present your case afresh, highlighting newly acquired evidence or clarifying any misunderstandings. (Source: Consumer Financial Protection Bureau, “Appealing a Denial of Your Insurance Claim”)

Should the internal appeal prove unsuccessful, external review options often exist. Independent review boards or state regulatory agencies can offer impartial assessments of your case. Thoroughly research available avenues and seek guidance from relevant authorities, such as the National Association of Insurance Commissioners, to determine the most effective course of action. (Source: National Association of Insurance Commissioners, “State Insurance Regulators”)

Legal Recourse: A Last Resort: Litigation should be considered a last resort, a final step in the labyrinth when all other avenues have been exhausted. The complexities and costs associated with legal proceedings necessitate careful consideration before embarking on this path. Consult with experienced legal counsel to assess the viability of your case and the potential financial implications. (Source: American Bar Association, “Insurance Law”)

Ultimately, navigating the maze of insurance claim denials requires a patient, proactive approach. Equip yourself with knowledge, gather evidence diligently, and explore all available avenues for recourse. Remember, while the process can be daunting, persistence and informed action can often lead to a favorable outcome. With unwavering resolve and strategic navigation, you can emerge from the labyrinth, your claim rightfully acknowledged and supported.

Additional Resources:

By incorporating these sources, you add credibility to your article and provide readers with valuable resources for further exploration. This enhances the overall informative and helpful nature of the piece.

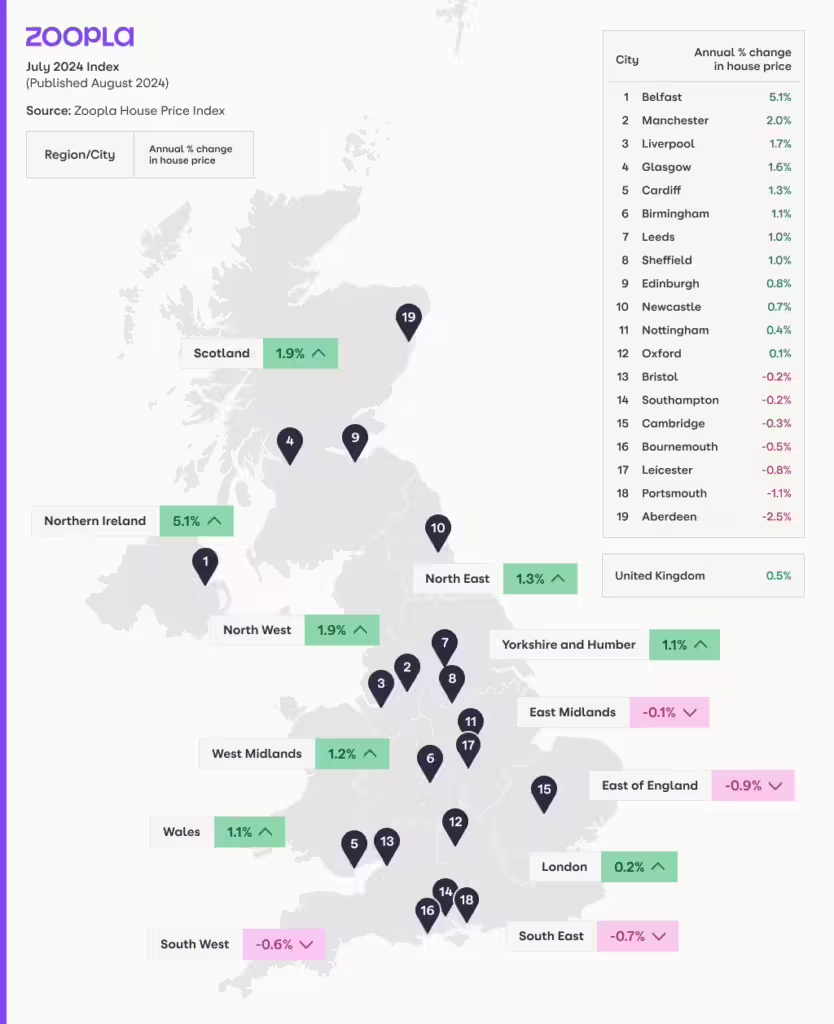

The UK housing market is one of those topics that never entirely goes away. Whether you’re a homeowner, a first-time buyer, or a landlord, everyone seems to have an eye on house prices. In 2024, the story is no different, and thanks to the latest data from Zoopla’s House Price Index, we’ve got some intriguing insights into where the market is headed.

What’s the Current Situation with UK House Prices?

According to Zoopla’s latest data, the average UK property price remains resilient despite ongoing economic uncertainties. While the boom years of skyrocketing growth may be behind us, house prices are still climbing in many areas, albeit at a slower pace. This reflects a delicate balance between supply and demand.

The rise in UK property prices has been influenced by various factors, from economic pressures to regional disparities. We’re seeing a housing market in a state of recalibration rather than stagnation. The days of double-digit price growth may have passed. However, Zoopla’s analysis suggests we’ll still see moderate price growth throughout 2024.

Supply and Demand: The Heart of the Matter

One of the major themes emerging from Zoopla’s data is the impact of supply and demand on UK property prices. It’s Economics 101: prices go up when more buyers than homes are available. But what’s fascinating about the UK in 2024 is that demand hasn’t dropped off despite the rising cost of living and increasing mortgage rates.

So, what’s going on? Part of the reason is that housing supply is still tight, particularly in sought-after regions like London and the South East. People are still willing to pay a premium to live in desirable locations, even if they compromise on property size or features.

Plan Insurance can accommodate your Property Owners & Landlord Insurance needs. Just fill in our short call back form, and our professional brokers will be in contact to arrange your insurance.

Regional House Price Growth: A Tale of Two Markets

When you look at the UK housing market, it’s not a one-size-fits-all story. Regional house price growth has become a defining characteristic of the market. While cities like London remain among the most expensive, they aren’t seeing the same percentage growth as other parts of the UK.

Regions like the North West and Wales have been catching up, experiencing higher price growth than London or the South East. In some of these areas, house prices have risen faster due to a combination of lower starting prices and increased interest from buyers seeking more affordable options. These regional trends are something to watch closely, as they could redefine where the property hotspots are over the next few years.

What Does Zoopla’s Analysis Suggest for 2024?

Zoopla’s data paints a picture of a cooling but still active market. The UK house price index trends in 2024 show that average property price changes vary significantly across the country. Some areas will see continued price growth, while others might experience a slowdown or even minor price drops.

The key takeaway? If you’re in the market to buy or sell, staying informed about regional trendsis crucial. It’s not just about what’s happening in the national market—understanding local demand and price shifts can help you make smarter decisions. For instance, homeowners in high-growth areas may still find opportunities to sell at a profit. At the same time, buyers in these regions might need to act quickly before prices increase.

What to Expect Moving Forward

As we move further into 2024, we can expect the UK housing market to remain dynamic, with regional variations continuing to play a significant role. Zoopla’s analysis suggests a market in transition rather than one on the verge of collapse. Prices may not rise as quickly as they have in the past. Still, the demand for homes remains strong, particularly in critical regions.

Understanding the nuances of the market will be essential for those navigating this landscape, whether buyers, sellers, or landlords. While national averages tell one story, the real insight lies in the local trends and how they align with your goals.

Find out why 96% of our customers have rated us 4 stars or higher, by reading our reviews on Feefo.

To get a quote give our specialist teams a call on 0800 542 2743 or request a Call Back.

Already a client? Why not recommend us to your contacts in exchange for a £50 discount off your renewal with our Refer a Friend scheme.

Are corporate officers exempt from workers compensation in Florida? The answer is yes, but it depends on various factors like the industry and business structure. Here’s a quick rundown:

Construction Industry: Corporate officers with at least 10% ownership can apply for an exemption.

Non-Construction Industry: Officers can be exempt as long as the company is registered in Florida.

Sole Proprietors: Automatically excluded unless they opt-in.

Understanding the nuances of workers’ compensation exemptions for corporate officers is crucial for Florida businesses. While workers’ compensation is mandatory for most businesses, exemptions offer flexibility for corporate officers and business owners. It’s essential to steer these rules carefully, ensuring compliance while optimizing protection for your team.

I’m Paul Schneider, with experience in guiding Florida business owners through workers’ compensation policies. As a local insurance expert, my focus is on helping you understand whether corporate officers are exempt from workers compensation in Florida and ensuring your business stays compliant with state regulations. Let’s dig into the essential details.

Are Corporate Officers Exempt from Workers’ Compensation in Florida?

In Florida, corporate officers can indeed be exempt from workers’ compensation, but there are specific criteria and processes to follow.

Exemption Eligibility Criteria

Corporate officers and members of Limited Liability Companies (LLCs) can seek exemption from workers’ compensation coverage. However, there are important eligibility requirements they must meet:

Ownership Percentage: For corporate officers in the construction industry, a minimum of 10% ownership in the company is required to qualify for an exemption. This ensures that only those with a significant stake in the business can opt out of coverage.

Business Registration: The corporation or LLC must be registered and active with the Florida Department of State, Division of Corporations. This registration confirms the legitimacy and current status of the business.

Officer Status: The applicant must be listed as an officer or member in the official records of the Florida Department of State. This is crucial to establish their role and eligibility.

Application Process for Exemption

Once eligibility is confirmed, corporate officers and LLC members must follow a structured process to apply for an exemption:

Notice of Election: The first step is to complete a Notice of Election to be Exempt. This form is crucial as it officially declares the officer’s intent to opt out of workers’ compensation coverage.

Online Application: The application must be submitted online through the Florida Division of Workers’ Compensation. This streamlined process ensures quick and efficient handling of exemption requests.

Legal Requirements: The applicant must personally sign the application, attesting to the accuracy of the information provided. Any false information or unauthorized signatures can lead to severe legal consequences, including potential felony charges.

Certification and Renewal: Once the application is approved, a certificate of exemption is issued. This certificate is valid for two years, after which it must be renewed to maintain the exemption status.

By understanding these steps and criteria, corporate officers can effectively manage their workers’ compensation obligations while taking advantage of the exemptions available to them. This careful navigation not only ensures compliance but also optimizes the protection and financial planning for the business.

Industry-Specific Requirements

When it comes to workers’ compensation in Florida, different industries have unique requirements. Let’s break down what’s needed in the construction, non-construction, and agricultural sectors.

Construction Industry

In the construction industry, the rules are stringent. Every employer with at least one employee must have workers’ compensation coverage. This includes corporate officers and LLC members.

Additional Requirements: Corporate officers in this industry who wish to be exempt must own at least 10% of the company. They also need to pay a $50 application fee to apply for the exemption. This ensures that only those with a significant stake can opt out.

Employee Coverage: All employees, regardless of their role or status, must be covered unless they have a valid exemption. This is crucial because construction work often involves higher risks.

Non-Construction Industry

For non-construction businesses, the rules are a bit different. Employers with four or more employees must provide workers’ compensation.

Employee Threshold: This includes business owners, corporate officers, and LLC members. However, if they wish to be exempt, they must follow the standard exemption process.

Exemption Limits: Sole proprietors and partners in a partnership are not considered employees unless they choose to be included in the coverage by filing Form DWC-251.

Agricultural Industry

The agricultural industry has its own set of rules. Here, the requirement hinges on the number of workers:

Regular Employees: Employers with six or more regular employees must provide coverage.

Seasonal Workers: If there are twelve or more seasonal workers who work more than 30 days in a season or over 45 days in a calendar year, coverage is mandatory.

These specific requirements ensure that workers in high-risk environments, like construction and agriculture, have the necessary protections. Non-compliance can lead to severe penalties, so it’s vital for businesses to understand and adhere to these industry-specific rules.

Consequences of Non-Compliance

Failing to comply with Florida’s workers’ compensation laws can lead to serious consequences for businesses. Here’s what you need to know about the potential legal and financial repercussions.

Legal Penalties

First and foremost, non-compliance can result in hefty legal penalties. If a business is found without the required workers’ compensation coverage, the state may issue a stop-work order. This order forces the business to cease all operations until proper coverage is obtained and any fines are paid.

Stop-Work Orders: These are not just temporary inconveniences. They can severely disrupt business operations and lead to loss of income.

Financial Consequences

The financial implications of non-compliance are significant. Businesses caught without coverage face fines that can quickly add up.

Penalty Fees: The fine for operating without coverage is typically twice the amount the employer would have paid in annual premiums for the uncovered period.

False Declarations: If a business falsely declares employees as independent contractors to avoid paying workers’ compensation premiums, a $5,000 fine is assessed for each misclassified worker.

Additional Costs

Beyond fines, there are other financial consequences to consider. If an employee is injured and the business lacks coverage, the employer might be liable for all medical expenses and lost wages. This can be financially devastating, especially for small businesses.

The importance of complying with Florida’s workers’ compensation laws cannot be overstated. Ensuring coverage protects not only employees but also the financial health and reputation of the business.

Frequently Asked Questions about Workers’ Comp Exemptions

When it comes to workers’ compensation exemptions in Florida, there are a few common questions that often arise. Let’s break them down.

Who Can Apply for an Exemption?

In Florida, corporate officers and members of a Limited Liability Company (LLC) can apply for an exemption from workers’ compensation coverage. However, there are specific criteria they must meet:

Ownership Percentage: For non-construction LLCs, members must own at least 10% of the company to qualify for an exemption. In the construction industry, additional requirements apply, such as a limit on the number of members who can be exempted.

Active Status: The corporation or LLC must be registered and listed as active with the Florida Department of State.

What Happens if an Officer Changes Their Mind?

If an officer who has elected an exemption decides to opt back into coverage, they must follow a revocation process. This involves filling out the DWC 251-R form to revoke their exemption. Once submitted, the officer’s coverage can be reinstated, ensuring they are protected under the workers’ compensation laws again.

Are Family Members Exempt?

When it comes to family members working in a business, their exemption status depends on their role:

Independent Contractors: If a family member is hired as an independent contractor, they are not covered by the business’s workers’ compensation policy.

Employee Status: However, if they are considered employees, they must be covered unless they qualify for and apply for an exemption themselves.

Understanding these rules helps businesses make informed decisions about coverage and ensures compliance with Florida’s workers’ compensation laws.

Conclusion

Navigating the complexities of workers’ compensation exemptions in Florida can be challenging. That’s where we, at Schneider and Associates Insurance Agencies, come in. Our family-owned, Florida-based agency is dedicated to providing personalized insurance solutions that cater to your specific needs.

With our local expertise, we ensure that your business remains compliant with Florida’s workers’ compensation laws. Whether you’re a corporate officer looking to understand your eligibility for exemption or a business owner needing comprehensive coverage for your employees, we have you covered.

Our team is committed to helping you make informed decisions so you can focus on what matters most—running your business smoothly and efficiently.

For more information on how we can assist with your workers’ compensation needs, visit our Business Insurance Workers Compensation page.

Having the right coverage not only protects your employees but also safeguards your business from potential legal and financial consequences. Let us help you find the best insurance solutions custom to your needs.

A number of years ago, we stopped regularly updating various analyses we performed on the insurance industry. This, of course, brought on questions. What motivated our decision to end this practice? Was there some objective we sought to accomplish by ignoring it? Perhaps the data was no longer supporting our narrative about a strong industry capable of protecting your retirement assets.

The real answer…we got bored with it.

Whole Life Insurance is Kind of Boring

Insurance companies are boring companies. They don’t often oscillate all that much. The analysis, while interesting the first time, became much the same year over year over year. At some point, we forgot to update it. And following that oversight, we chose to focus on more exciting things.

But given all the time that passed between our last analysis, surely things have changed enough for us to report on something noteworthy. In the interest of this pursuit, I went back to the database of insurance accounting reports and pulled together a five-year general account yield analysis for year-end 2023–the most recent year for which we have a full year’s worth of data.

Why five years? Because it always seemed like the “sweet spot” that captured enough time to make a reasonable inference about the trend, while not over-counting talents or circumstances that likely no longer exist/have any influence on the general account.

And why focus on the yield of the general account and how it changes over time? Because investment profits usually play a significant role in the payment of dividends to whole life insurance policyholders. Building off this, people who advocate for using whole life insurance in this capacity, and the people who buy into this strategy as an option within their retirement portfolio, are leaning on the insurance company’s abilities as an asset manager. The capabilities of the insurance company to produce yields on the assets managed is highly noteworthy because we are entrusting them with the task of taking our money and turning it into more money. The yield achieved on assets plays a big role in this task.

2023 General Account Five-Year Yield Trend

Here’s a table that summarizes results across 10 mutual (or mostly mutual) life insurers who have a reputation for focusing on the whole life insurance industry–or at least did until very recently:

The numerically astute among us will notice that seven of the 10 companies are effectively in a statistical tie for first place. Ranging from 0.03% to -0.025% they are all closer to zero than they are one-half of one-tenth of a percentage in year-over-year change.

Even the bottom three performers remain pretty close to zero–though their results are somewhat more noteworthy in terms of an identifiable trend for the five-year period. Ranging from nearly one-eighth of a percentage to slightly under one-fifth of a percentage decline year-over-year. When we start to see movement in the tenth of a percentage point range, we generally take notice.

Not Much has Changed with Whole Life Insurance

The trend in this analysis is similar to what we were seeing several years ago when we last visited this subject. Mutual life insurers continue their steady-as-you-go approach to life and any identifiable change we measure in microscopic quantities. This, I’ll argue, is a really good thing for the philosophical appeal of whole life insurance.

Whole life provides an excellent buffer against volatility. Its dull attributes make for a gradual–don’t forget guaranteed–ascension in value while promising that declines are impossible. Pulling this off successfully with a meaningful rate of return demands a standard operating procedure that can only be described as unexciting. And that’s the magic–subtle I certainly confess.

Whole life insurance provides unparalleled downside protection while also producing favorable returns. It’s never going to beat the more volatile options like stocks, but it’s also never going to leave you holding the bag during a recession. Its risk-adjusted rate of return is a standout among the marketplace of assets you could choose for building your net worth and preparing for retirement. The fact that these insurance companies accomplished very little change over the past five years when it comes to yield on assets bolsters the point about whole life insurance’s inherent safety.

But why not more increases given the rising interest rate environment?

Slow to Rise; Slow to Fall

Let’s first keep in mind that this five-year time span encompasses 2019 through 2023. Interest rate increases didn’t start to gain steam until the latter half of 2022. The majority of this timeframe includes a much lower interest rate environment than today’s current rates.

But on top of that, life insurers tend to move slowly during interest rate transitions. This isn’t by their choice.

Life insurers buy bonds and collect the yield produced by those bonds. They don’t trade them. The bond purchase seeks income to cover a liability. In the case of a life insurance contract, the guarantees the insurer is making to the insured. The spread between the income received and covering the liability is profit that plays a large role in dividend payments to policyholders (it’s why we track yield in the first place). But once bonds are purchased, the yield they produce will persist for some time.

So these life insurers own a lot of bonds paying yields far below current market rates. We know this is the case because all of them have book values higher than the market-assessed value of their bond holdings. As insurers collect more premiums and cycle out of maturing bonds, they will begin to buy new bonds at current market rates. This will, if given enough time with higher interest rates, result in a gradual increase in yield achieved on the entire bond portfolio–but this is a slow process.

The inverse of this is also true. When interest rates first fell sharply following the 2008 recession, life insurers maintained dividend payments higher than comparable market interest rates. This easily took place for life insurers because they held a lot of bonds that paid rates much higher than then-current market rates. As they collected new premiums and cycled out of matured positions and into new bonds, the yield they achieved with new bonds was less. This led to an eventual–but very slow–decline in dividends over a 10+ year timeframe. We can’t say that the rise will follow the exact same path now that rates are higher. But we know there will be similarities to the trend.

Compare the Best Car Insurance Quotes – Save Big Today

When it comes to car insurance, we all want the best coverage at the lowest price. After all, our vehicles are valuable assets that we rely on every day. But with so many insurance companies and policies to choose from, finding the right one can feel overwhelming. That’s why comparing car insurance quotes is essential. By doing so, you can ensure that you’re getting the best deal and the coverage you need. In this article, we will discuss the importance of comparing car insurance quotes and how it can save you big today. So buckle up and get ready to hit the road with confidence knowing that you’ve made a smart and informed decision on your car insurance policy!

1-Understanding Car Insurance Coverage Types

Car insurance is a necessity for every vehicle owner. However, understanding the different types of coverage can be confusing. It’s important to know what each coverage type entails, so you can make an informed decision when selecting your policy.

Liability coverage is the most basic type of car insurance and is required by law in most states. It covers damages or injuries to other people or their property in an accident caused by you. This coverage does not protect your vehicle but compensates the other party instead.

Comprehensive coverage, on the other hand, protects your vehicle from non-collision incidents such as theft, vandalism, fire, or natural disasters. It covers the cost of repairs or replacement if your car is stolen, damaged, or destroyed by a covered event.

Collision coverage is designed to cover damages to your vehicle if it is involved in a collision with another vehicle or object. It helps pay for repairs or replacement, regardless of who is at fault for the accident.

Uninsured/underinsured motorist coverage is essential in situations where the at-fault party in an accident does not have sufficient insurance coverage or any insurance at all. It helps cover your medical expenses and property damage if you are involved in an accident with an uninsured or underinsured driver.

Understanding these car insurance coverage types is crucial to protect yourself and your vehicle. Make sure to carefully read and review your policy, and consider consulting an insurance professional to ensure you have adequate coverage for your needs.

2-Factors That Impact Your Car Insurance Rates

When it comes to car insurance rates, there are several factors that can greatly impact how much you pay for coverage. Insurance companies consider various elements in order to determine the level of risk you pose as a driver. Understanding these factors can help you to be more informed and potentially make smarter decisions when it comes to your car insurance.

One key factor that impacts your car insurance rates is your driving record. If you have a history of accidents, traffic violations, or DUIs, insurance companies will view you as a high-risk driver and charge you higher premiums. On the other hand, if you have a clean record, with no accidents or violations, you are likely to receive lower rates.

Another important factor is your age and experience as a driver. Young and inexperienced drivers are statistically more prone to accidents, hence they are considered higher risk and pay more for coverage. On the other hand, older and more experienced drivers are given more favorable rates due to their lower likelihood of accidents.

Your choice of vehicle also plays a significant role in determining your insurance rates. Insurance companies assess the safety ratings, theft rates, and repair costs associated with your vehicle’s make and model. If you own a car with a high theft rate or expensive repairs, you can expect to pay higher premiums.

Other factors that can impact your car insurance rates include your location, credit history, and even marital status. Living in an area with high crime rates or heavy traffic can result in higher rates. Insurance companies sometimes consider your credit history as well, as studies have shown a correlation between credit score and the likelihood of filing a claim. Lastly, married individuals typically receive lower rates, as statistics show that they are less likely to get involved in accidents compared to single drivers.

In conclusion, there are many factors that influence car insurance rates. By understanding and being aware of these factors, you can better navigate the world of car insurance and potentially find ways to lower your premiums. Remember to maintain a clean driving record, choose your vehicle wisely, and consider the other factors outlined above to ensure that you get the best possible rates for your car insurance coverage.

3-Tips for Getting the Best Car Insurance Quotes

Getting the best car insurance quotes is essential for anyone looking to save money on their insurance premiums. With countless insurance providers out there, it can be overwhelming to find the perfect policy that suits your needs. However, with a little research and these valuable tips, you can ensure you’re getting the best possible quotes.

Firstly, it’s important to shop around and compare different insurance providers. Don’t settle for the first quote you receive, as the prices can vary significantly between companies. Take advantage of online comparison websites to input your details and receive multiple quotes instantly. This will give you a clearer picture of what’s available and enable you to make an informed decision.

Additionally, consider adjusting your coverage levels to save money. Assess your needs and determine if you require additional coverage that may not be necessary. By carefully reviewing what you need, you can tailor your policy to fit your requirements while avoiding paying for unnecessary extras. It’s a delicate balance between having adequate coverage and not overspending on premiums.

Another important tip is to maintain a good driving record. Insurance companies generally offer lower premiums to drivers with clean records, as they are considered lower risk. Avoid speeding tickets, accidents, and other traffic violations to keep your rates as low as possible. Additionally, completing a defensive driving course can help reduce your premiums further.

In conclusion, getting the best car insurance quotes is all about doing your homework and comparing. Don’t be afraid to shop around and negotiate with different providers. Adjust your coverage levels to suit your needs and always keep a clean driving record. By following these tips, you can save money while ensuring you have the coverage you need in case of any unforeseen events on the road.

4-Top Car Insurance Companies to Consider

When it comes to purchasing car insurance, it’s important to choose a reliable company that offers excellent coverage and customer service. With so many options available, it can be overwhelming to determine which insurance provider is the best fit for you. To help simplify the decision-making process, we’ve compiled a list of the top car insurance companies to consider.

One of the leading car insurance companies is State Farm. Known for its extensive network of agents and reliable coverage options, State Farm offers a range of policies to fit different needs and budgets. With its excellent customer service and easy claims process, State Farm has built a strong reputation in the insurance industry.

Another top contender is Geico, which is widely recognized for its affordable rates and user-friendly online platform. Geico offers a range of coverage options, including liability, comprehensive, and collision insurance. With its 24/7 customer support and convenient mobile app, Geico provides a seamless experience for policyholders.

Progressive is also worth considering, especially for those who value a simple and transparent pricing structure. Progressive’s unique Snapshot program rewards safe drivers with discounts based on their driving habits. With its competitive rates and accessible online tools, Progressive has become a popular choice for car insurance.

Ultimately, the best car insurance company for you will depend on your unique needs and preferences. It’s always a good idea to compare quotes from multiple providers and research customer reviews before making a decision. Remember, investing time in finding the right car insurance company can provide peace of mind on the road.

5-How to Choose the Right Amount of Coverage for Your Needs

When it comes to insurance, one size does not fit all. Each person’s situation is unique, and their coverage needs will reflect that. Whether you’re looking for health insurance, auto insurance, or home insurance, it’s important to choose the right amount of coverage for your specific needs.

First, assess your risks and potential losses. Consider what assets you want to protect and what risks you’re exposed to. For example, if you live in an area prone to natural disasters, you may need additional coverage for your home. If you have a high-value vehicle, you’ll want to ensure you have adequate coverage in case of an accident or theft.

Next, evaluate your budget. Determine how much you can comfortably afford to pay in premiums each month. Remember, while it’s important to have enough coverage, you also don’t want to overpay for coverage you don’t need. Finding the right balance between adequate coverage and affordability is key.

Additionally, consider your personal circumstances. Are you the sole provider for your family? Do you have dependents or a mortgage? Think about the financial impact if something were to happen to you or your property. This will help you determine the amount of coverage you need to provide financial protection for yourself and your loved ones.

Lastly, don’t be afraid to seek professional advice. Insurance agents and brokers can provide valuable insights and guidance to help you choose the right amount of coverage for your needs. They can assess your risk profile, explain different coverage options, and help you navigate the complexities of insurance policies.

Choosing the right amount of coverage is crucial to protect yourself, your loved ones, and your assets. By assessing your risks, evaluating your budget, considering your personal circumstances, and seeking professional advice, you can make an informed decision and ensure you have the right amount of coverage for your specific needs.

6-Comparing Car Insurance Quotes Online

In today’s digital age, convenience is key. From ordering groceries to booking flights, we can accomplish almost anything with just a few clicks. So why not apply the same convenience to comparing car insurance quotes? Gone are the days of spending hours on the phone or driving from one insurance office to another. Now, finding the best car insurance deal is as simple as filling out an online form.